Nifty 50 closed at 25,005.50 (32.4, 0.1%), BSE Sensex closed at 81,548.73 (123.6, 0.2%) while the broader Nifty 500 closed at 23,102.65 (28.5, 0.1%). Market breadth is in the red. Of the 2,551 stocks traded today, 1,190 were gainers and 1,313 were losers.

Indian indices fluctuated between gains and losses throughout the session but ended marginally higher. The Indian volatility index, Nifty VIX, fell around 1.7% and closed at 10.2 points. Kalpataru Projects International closed 2.3% higher as it secured new orders worth Rs 2,720 crore across its power transmission & distribution and buildings businesses.

Nifty Smallcap 100 and Nifty Midcap 100 closed flat. Nifty Oil & Gas and BSE Power closed in the green. According to Trendlyne’s Sector dashboard, Forest Materials emerged as the best-performing sector of the day, with a rise of 4.1%.

European indices are trading in the green, except for Russia’s MOEX and RTSI. Major Asian indices closed mixed. US index futures are trading higher, indicating a positive start to the session, as investors await the release of the retail inflation print later today. Brent crude futures are trading lower amid weak demand in the US, following a week of strong gains driven by rising tensions in Russia and the Middle East.

Money flow index (MFI) indicates that stocks like Eicher Motors, Motherson Sumi Wiring, Kaynes Technology, and Netweb Technologies are in the overbought zone.

Shyam Metalics and Energy enters the crash barrier segment (road safety barriers), targeting 8-10% market share in FY26. The company plans to invest a total of Rs 100 crore across its Jharkhand and Odisha facilities to expand capacity and diversify products.

Veranda Learning Solutions' board approves the demerger of its commerce vertical as part of the ‘Veranda 2.0’ vision. The new entity, J.K. Shah Commerce Education, will handle all future commerce operations.

Tata Motors' arm Jaguar Land Rover (JLR) faces a cybersecurity incident affecting some data and forcing an extended system shutdown. The breach has reportedly disrupted production and sales, potentially costing up to £5 million (~Rs 59.7 crore) per day.

A Union Bank of India report indicates that India’s wholesale inflation likely turned positive in August, rising to 0.5% YoY from -0.6% in July. Food inflation, after two months of deflation, likely returned to the positive territory, with price increases observed across most sub-segments.

Wholesale inflation in India likely turned positive in August 2025, rising to 0.45 per cent year-on-year after recording a contraction of -0.58 per cent in July, according to a report by Union Bank of India (UBI).https://t.co/S2agRr6YBY

— businessline (@businessline) September 11, 2025Motilal Oswal initiates coverage on Bajaj Housing Finance (BHFL) with a 'Neutral' rating and a target price of Rs 120 per share. The brokerage notes BHFL’s strong position as the second-largest HFC with solid asset quality and AAA ratings. However, it warns that rising competition from banks could slow growth and put pressure on RoE. It expects AUM and net profit to grow at ~22% CAGR over FY26-28.

Prostarm Info Systems is rising as it receives a Rs 158.7 crore order to manage crime and criminal tracking network & systems (CCTNS) IT infrastructure across Maharashtra police establishments. The project includes supply, installation, commissioning, and maintenance of related peripherals.

Ambuja Cements is falling as 2.8 crore shares (1.2% stake), worth approximately Rs 1,546 crore, reportedly change hands in a block deal at an average price of Rs 552 per share.

HSBC Global upgrades NTPC to a 'Buy' rating with a higher target price of Rs 400. The brokerage notes that NTPC has resolved thermal project delays with the commissioning of two plants. The company has another 1.4 GW unit, which is due to be commissioned by FY26. The power company is testing battery integration with low-cost coal plants to boost grid stability, cut curtailments, and supply cheaper power to distributors.

HSBC Global Research upgrades Maharatna PSU stock #NTPC, sees 23% upside potential.

— NDTV Profit (@NDTVProfitIndia) September 11, 2025

Read ????https://t.co/IrK6pQg2qrApollo Micro Systems surges as its subsidiary, Apollo Defence Industries (ADIPL), signs a memorandum of understanding with Dynamic Engineering and Design, USA. The agreement involves technology transfer, co-development, and potential licensed production of rocket motors for BM-21 Grad rockets.

BSE and Angel One fall sharply as SEBI is reportedly preparing a consultation paper to end weekly F&O contracts and shift to monthly expiries. The regulator may also propose curbs on retail participation and same-day expiries across exchanges. The SEBI board is set to meet on September 12.

SpiceJet is rising as it reaches a settlement with Carlyle Aviation Partners, receiving $89.5 million (approximately Rs 790 crore) in cash and credits to fund aircraft maintenance and offset lease obligations.

A poll of economists suggests India’s retail inflation likely rose to 2.2% in August, up from July’s eight-year low of 1.6%. The increase is attributed to higher food prices from crop damage caused by excess rains, as well as a low base effect. Additionally, rising costs in services such as personal care and elevated gold prices are expected to push core inflation higher.

#India’s consumer price index (CPI)-based retail inflation rate is likely to have recorded an uptick in August to 2.18% from an eight year low of 1.55% in July, a Business Standard poll of nine economists show.@ShivaRajora7#foodprices#retailinflation#CPI#Inflation… pic.twitter.com/VSS3DpuOUX

— Business Standard (@bsindia) September 11, 2025

BEML is reportedly set to be upgraded from Miniratna to Navratna status, giving it a greater financial and operational flexibility.

Reliance Communications receives a show-cause notice from Central Bank of India over non-repayment of Rs 400 crore loans and violation of sanction terms. The company has 21 days to respond before its account is declared fraudulent and reported to the RBI.

Gujarat Fluorochemicals is falling as a gas leak at its Panchmahal plant reportedly kills one person and injures 12. The leak originated from a damaged pipeline releasing R-32 gas, a refrigerant used in air conditioning systems.

Nomura initiates coverage on Gail India with a 'Buy' rating and a target price of Rs 225. The brokerage notes that a tariff hike of over 20% could offer Gail a one-time boost and potentially surprise investors positively. It also highlights that recovery in the petrochemical segment is likely to begin from FY27, driving strong investor interest in the stock.

#MarketsWithMC | Nomura sees 30 percent upside for Gail India on one-time boost from tariff hike and petchem recovery

More Details ????? | #Nomura#GailIndia#Shareshttps://t.co/vrI1DY5j30— Moneycontrol (@moneycontrolcom) September 11, 2025

Tega Industries’ board approves a $1.5 billion (~Rs 13,216 crore) deal to acquire global mining consumables giant Molycop in partnership with Apollo Funds. Upon closure, Tega will hold a controlling stake, while Apollo Funds will retain a significant minority interest.

Adani Power is rising as it secures a letter of award (LoA) from MP Power Management (MPPMCL) to supply additional electricity from a new 800 MW ultra-supercritical thermal power plant in Madhya Pradesh. This takes the total awarded capacity to 1,600 MW, with a planned capex of Rs 21,000 crore.

ACME Solar Holdings is rising as it secures Rs 3,892 crore in project funding from State Bank of India (SBI) to develop a 400 MW firm and dispatchable renewable energy (FDRE) project in Barmer, Rajasthan.

Japan's Sumitomo Mitsui Banking Corp sells 3.2 crore shares of Kotak Mahindra Bank, in a block deal valued at Rs 6,256 crore. Meanwhile, major buyers in the deal include Abu Dhabi Investment Authority (ADIA), Goldman Sachs Bank Europe SE, Amundi Funds, and BlackRock Global Funds.

#ADIA, #Amundi, #GoldmanSachs among marquee buyers in Kotak Mahindra Bank block deal@senmeghnahttps://t.co/m0eR7WXajz

— CNBC-TV18 (@CNBCTV18Live) September 11, 2025

Kalpataru Projects International is rising as it secures new orders worth Rs 2,720 crore in power transmission and distribution (T&D) in India and overseas, and its buildings and factories (B&F) business in India.

Jupiter Wagons rises sharply as its subsidiary receives an order worth Rs 113 crore from the Ministry of Railways to supply 9,000 Linke Hofmann Busch (LHB) axles for FIAT-Indian Railways (IR) bogies.

Rail Vikas Nigam is rising as it secures an order worth Rs 169.5 crore from West Central Railway. The order involves building traction substations and related systems between Bina Junction and Ruthiyai station in the Bhopal Division, aimed at meeting a 3,000 metric tonne loading target.

Dr. Reddy's Laboratories signs a $50.5 million (Rs 445 crore) deal with Johnson & Johnson affiliate Janssen Pharmaceutica NV to acquire the anti-vertigo drug 'Stugeron'. The acquisition strengthens its central nervous system (CNS) portfolio in India and emerging markets by adding the antivertigo segment.

Nifty 50 was trading at 25,000.80 (27.7, 0.1%), BSE Sensex was trading at 81,217.30 (-207.9, -0.3%) while the broader Nifty 500 was trading at 23,112.90 (38.8, 0.2%).

Market breadth is surging up. Of the 2,066 stocks traded today, 1,374 were in the positive territory and 619 were negative.

Riding High:

Largecap and midcap gainers today include Waaree Energies Ltd. (3,739.80, 7.5%), Aurobindo Pharma Ltd. (1,109.20, 5.6%) and Bharat Heavy Electricals Ltd. (229.08, 4.1%).

Downers:

Largecap and midcap losers today include Gujarat Fluorochemicals Ltd. (3,629.30, -3.1%), Sona BLW Precision Forgings Ltd. (439.95, -2.2%) and Jindal Stainless Ltd. (761.20, -2.2%).

Movers and Shakers

31 stocks in BSE 500 are trading on high volumes today.

Top high volume gainers on BSE included Waaree Energies Ltd. (3,739.80, 7.5%), Aurobindo Pharma Ltd. (1,109.20, 5.6%) and Neuland Laboratories Ltd. (15,554, 5.1%).

Top high volume losers on BSE were Angel One Ltd. (2,216, -5.2%), Kama Holdings Ltd. (2,965, -1.8%) and Adani Power Ltd. (624.65, -1.5%).

Jupiter Wagons Ltd. (333.45, 4.5%) was trading at 23.8 times of weekly average. Ambuja Cements Ltd. (560.40, -1.1%) and Gujarat State Petronet Ltd. (310, 3.5%) were trading with volumes 18.2 and 16.8 times weekly average respectively on BSE at the time of posting this article.

BSE 500: highs, lows and moving averages

5 stocks took off, crossing 52 week highs, while 1 stock tanked below their 52 week lows.

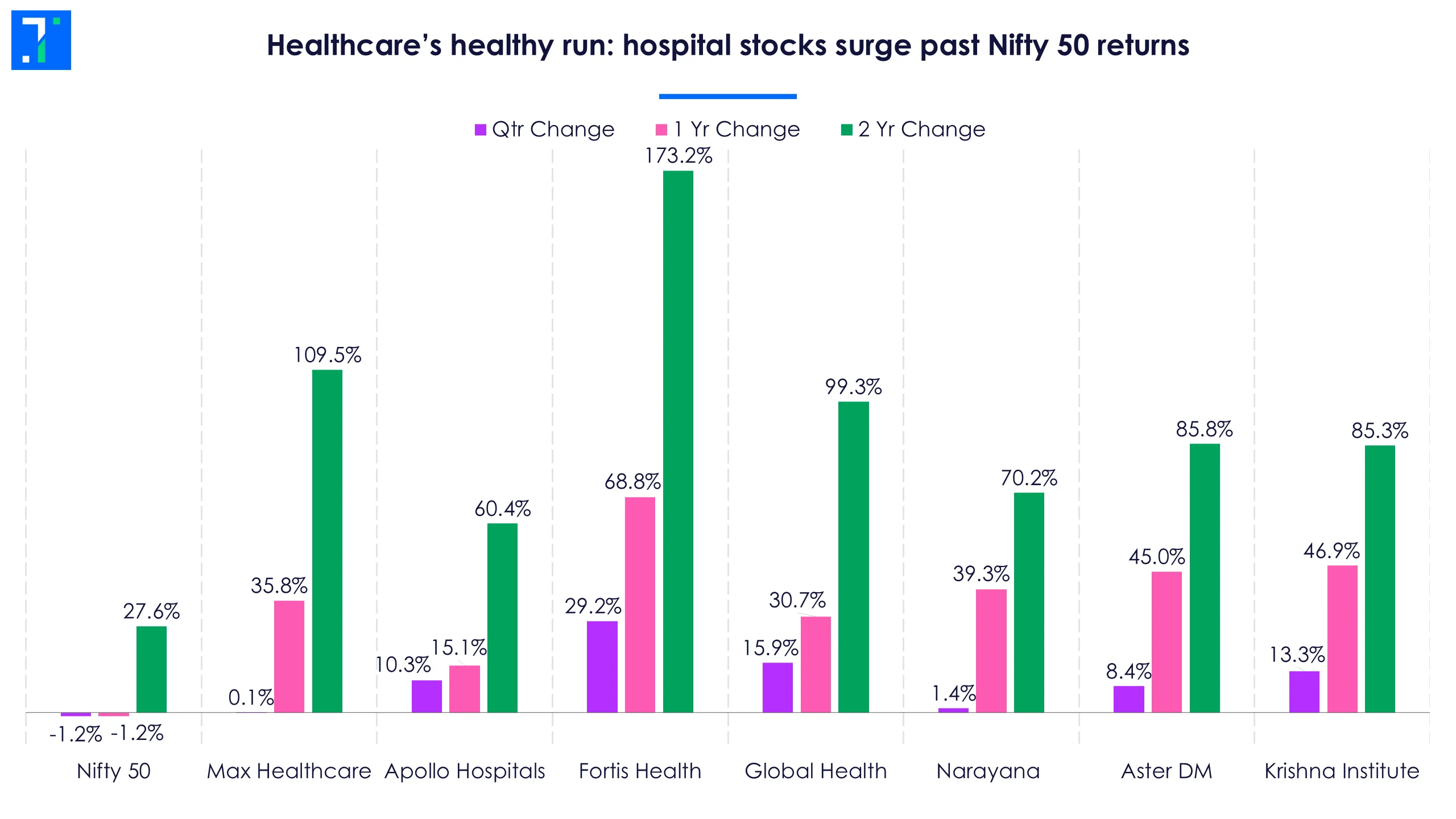

Stocks touching their year highs included - Fortis Healthcare Ltd. (965.95, -0.1%), Indian Bank (695.85, 0.5%) and Zydus Wellness Ltd. (2,551.90, 2.6%).

Stock making new 52 weeks lows included - United Breweries Ltd. (1,794, -0.3%).

31 stocks climbed above their 200 day SMA including Bharat Heavy Electricals Ltd. (229.08, 4.1%) and Firstsource Solutions Ltd. (365.35, 2.5%). 8 stocks slipped below their 200 SMA including Whirlpool of India Ltd. (1,330, -2.9%) and Ola Electric Mobility Ltd. (57.98, -2.3%).