By Ruchir SankhlaThe Nifty 50 kicked off the new month on a bearish note, closing 0.7% lower on June 1. The index failed to hold onto any early momentum as aggressive selling in banking, auto, and FMCG heavyweights dragged the broader market down.

The trigger for today's market slide was a sharp escalation in geopolitical rhetoric. Over the weekend, US Defence Secretary Pete Hegseth warned that Washington is fully prepared to resume military strikes on Tehran if the fragile ceasefire negotiations collapse. This aggressive stance reignited fears of a broader conflict and a potential spike in crude oil prices, forcing investors to take money off the table.

Here at home, domestic headwinds added fuel to the fire. Inflation concerns intensified after the India Meteorological Department (IMD) projected this year's southwest monsoon rainfall at just 90% of the long-period average, signalling a potentially deficient season. Adding to the bearish mood, Foreign Portfolio Investors (FPIs) remained net sellers in May, pulling out Rs 32,963 crore and keeping market sentiment highly cautious.

Dr V K Vijayakumar, Chief Investment Strategist at Geojit Investments, said, "Poor earnings growth in India, much superior earnings growth in countries like the US, Japan, South Korea and Taiwan and the strong AI-related trade in these countries, particularly in South Korea and Taiwan, contributed significantly to the FPI selling in India.” Looking ahead, market participants are bracing for a volatile week and will be watching the RBI’s bi-monthly policy meeting from June 3 to June 5.

Building on last week's momentum of six successful IPOs, the primary market remains highly active. This week is set to feature seven new issue openings alongside four market debuts.

Six SME IPOs hit the market last week

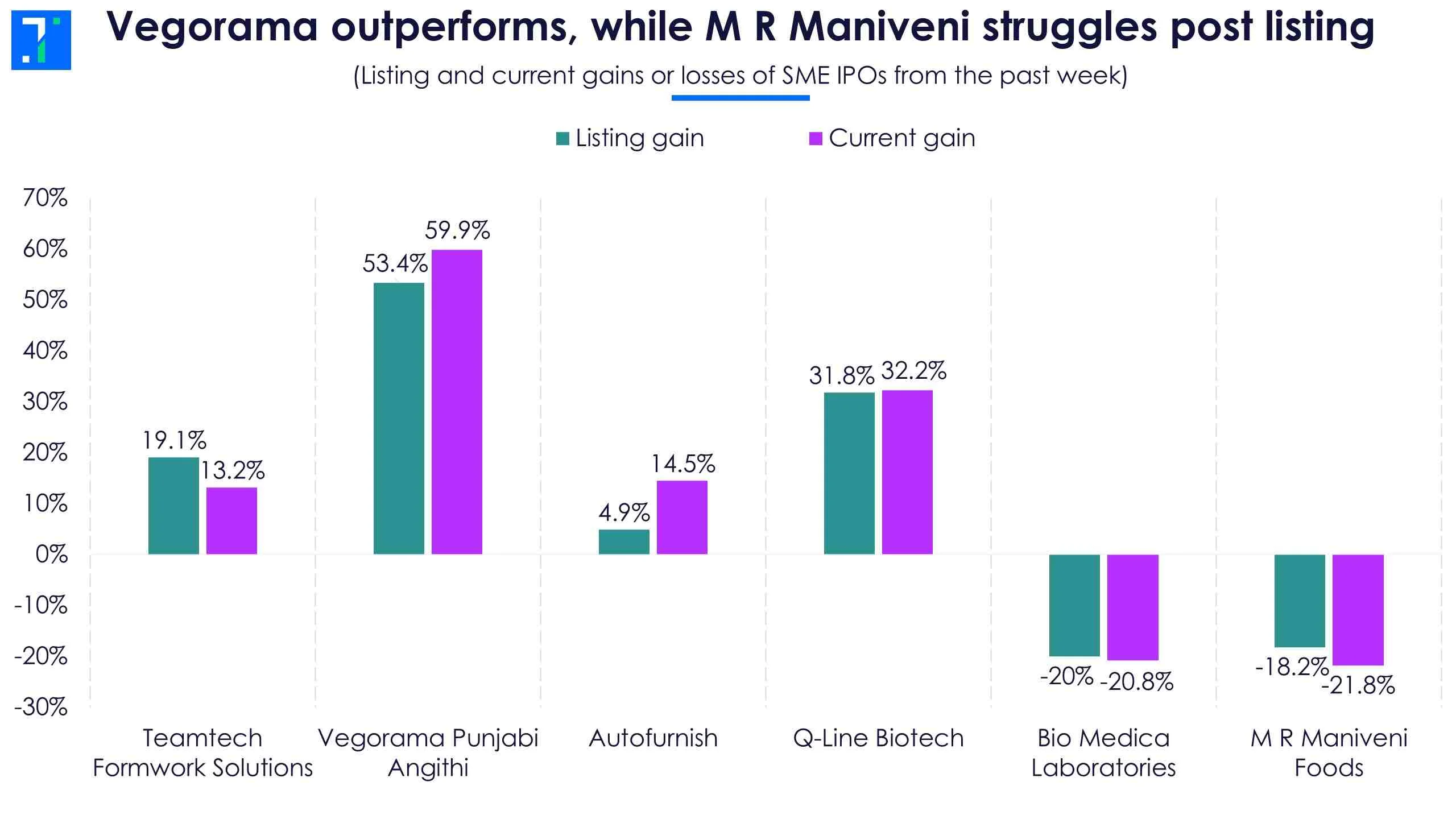

Teamtech Formwork Solutions, a Telangana-basedconstruction equipment manufacturer, made a strong debut on May 26. The Rs 50.1 crore IPO was subscribed 6.6x and listed at a 19.1% premium to its issue price of Rs 63. The company plans to use the proceeds to fund working capital requirements and business growth. The stock is currently trading 13.2% above its issue price.

Vegorama Punjabi Angithi, an operator of North Indian quick-service restaurants and cloud kitchens, made a strong debut on May 27. The Rs 38.4 crore IPO was subscribed 36.9x and listed at a 53.4% premium to its issue price of Rs 77. The company plans to use the proceeds to expand restaurant outlets, set up a central kitchen, upgrade cloud kitchens, and fund working capital needs. The stock is currently trading 59.9% above its issue price.

Autofurnish, an automotive accessories manufacturer, made a muted debut on May 29. The Rs 14.6 crore IPO was subscribed 1.2x and listed at a 4.9% premium to its issue price of Rs 41. The company plans to use the proceeds to purchase machinery, support working capital requirements, and meet listing expenses. The stock is currently trading 14.5% above its issue price.

Vegorama outperforms, while M R Maniveni struggles post listing

Bio Medica Laboratories, a manufacturer of pharmaceutical formulations, made a weak market debut on May 29. The Rs 52.4 crore IPO was subscribed 2.2x and listed at a 20% discount to its issue price of Rs 139. The company plans to use the proceeds to repay debt, set up a new manufacturing facility, and meet general corporate requirements. The stock is currently trading near its listing price.

Q-Line Biotech, ahealthcare diagnostics company, made a strong debut on May 29. The Rs 214.5 crore IPO attracted strong investor demand and listed at a 31.8% premium to its issue price of Rs 343. The company plans to use the proceeds for working capital needs, debt repayment, and general corporate purposes. The stock is trading 32.2% above its issue price.

M R Maniveni Foods, a pulses milling and processing company, made a weak debut on June 1. The Rs 27 crore IPO was subscribed 1.2x and listed at an 18.2% discount to its issue price of Rs 52. The company plans to use the proceeds to set up a new factory, purchase plant and machinery, and meet general corporate requirements. The stock is currently trading around 21.8% below its issue price.

From jewellery to chemicals: Four IPOs head for listing

Four SME IPOs are set to list this week, while no mainboard IPOs are scheduled.

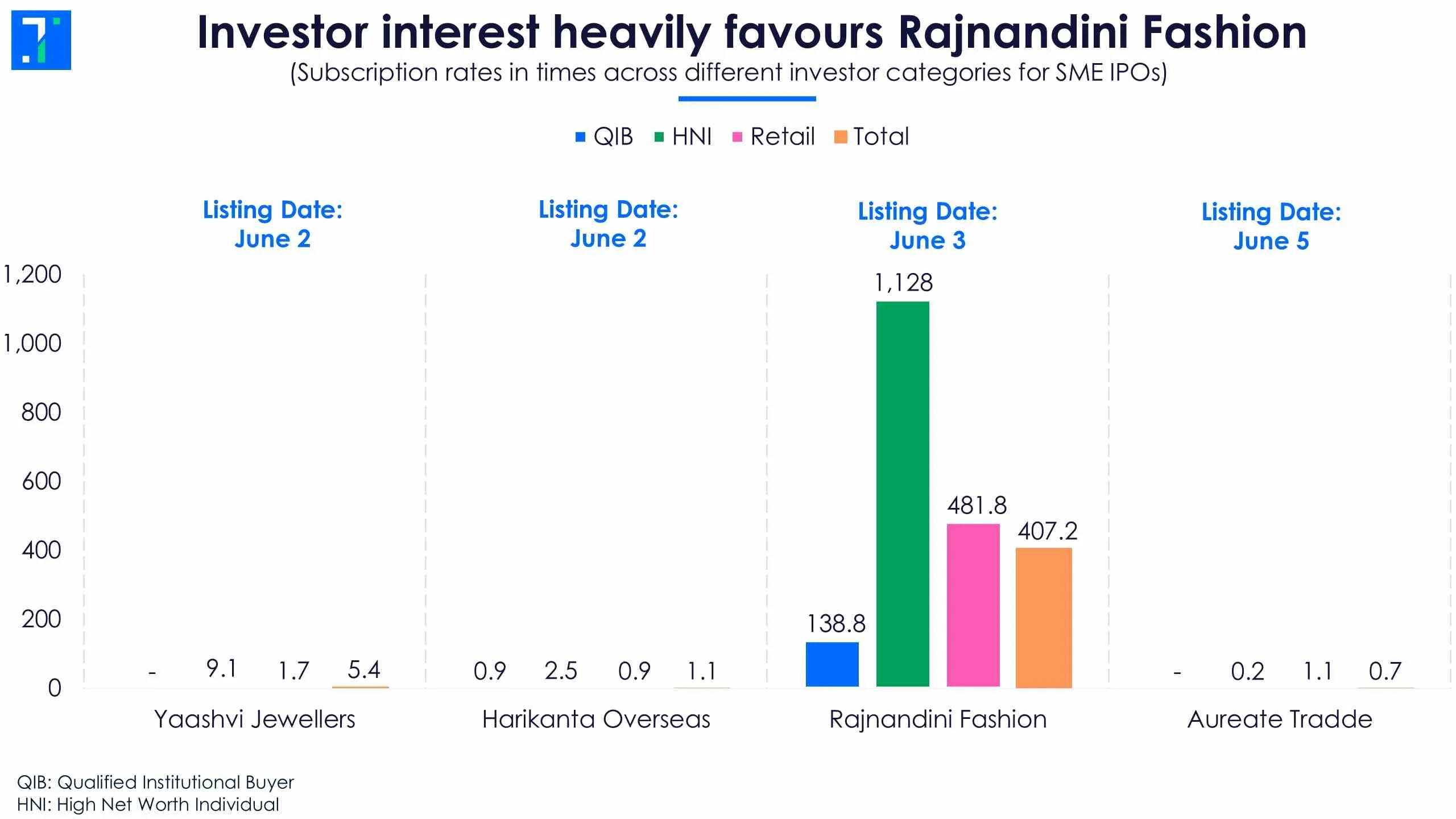

Yaashvi Jewellers, a Jaipur-based gold jewellery manufacturer, opened its Rs 43.9 crore IPO for subscription on May 25 and closed on May 27. The offering consisted entirely of a fresh issue of 52.9 lakh shares at a fixed price of Rs 83 per share. The issue saw healthy investor interest with an overall subscription of 5.4x, supported by high net worth individuals (HNIs). The company plans to use the proceeds to fund inventory purchases, address its working capital requirements, and meet general corporate expenses. The shares will list on June 2.

Harikanta Overseas, a Surat-based fabric manufacturer, opened its Rs 24.3 crore IPO for subscription on May 20 and closed on May 27. The offering consisted entirely of a fresh issue of shares at a price band of Rs 86–91. The issue saw an overall subscription of 1.1x. The company plans to use the proceeds for capital expenditure on factory premises, procurement of new machinery, and general corporate purposes. The shares will list on June 2.

Investor interest heavily favours Rajnandini Fashion

Rajnandini Fashion, an apparel manufacturer, opened its Rs 18.2 crore IPO for subscription on May 26 and closed on May 29. The offering consisted entirely of a fresh issue of 28.9 lakh shares at a price band of Rs 59–63. Driven by strong market enthusiasm, the issue was oversubscribed at 407.2x, backed by HNI investors. The company plans to use the funds to set up a new manufacturing facility, repay a portion of its debt, and meet working capital requirements. The stock will list on June 3.

Aureate Tradde, a Mumbai-based industrial materials and green technology distributor, opened its Rs 27.3 crore IPO for subscription on May 29 and will close on June 2. The offering consists entirely of a fresh issue of 39 lakh shares at a fixed price of Rs 70 per share. As of the second day, the issue saw an overall subscription of 0.7x. The company plans to use the net proceeds toward funding its working capital needs, prepaying outstanding borrowings, and for general corporate expenses. The shares will list on June 5.

IPO pipeline broadens with two mainboard launches

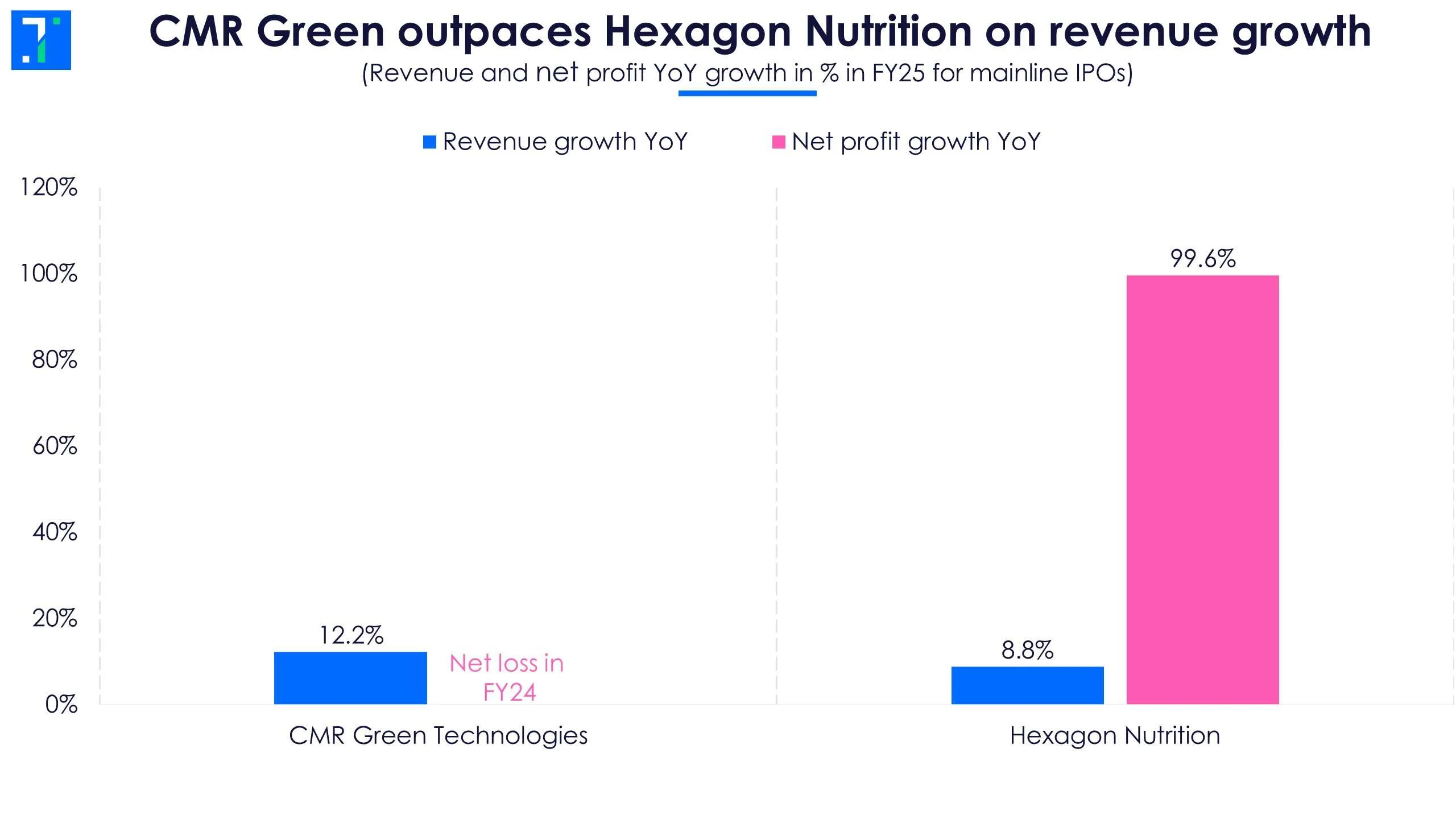

CMR Green Technologies, a non-ferrous metal recycler, plans to raise Rs 630.9 crore. The IPO will run from June 3 to June 5 at a price band of Rs 182–192. The firm will list on June 10 and, with the issue being entirely an Offer for Sale (OFS) of 3.3 crore shares, aims to gain the brand visibility and liquidity advantages of listing on the exchanges.

Hexagon Nutrition, a healthy foods and nutrient mixes manufacturer, plans to raise Rs 138.9 crore. The IPO will run from June 5 to June 9 at a price band of Rs 42–45. The firm will list on June 12 and, consisting entirely of an OFS of 3.1 crore shares, intends to achieve the strategic benefits of getting listed on the public stock exchanges.

CMR Green outpaces Hexagon Nutrition on revenue growth

Five SME IPOs also plan to open for subscription.

Merritronix, anelectronics parts manufacturer, plans to raise Rs 70 crore. The IPO will run from June 1 to June 3 at a price band of Rs 141–149. The firm will list on June 8 and plans to use the proceeds to purchase new factory machinery and equipment, fulfil working capital demands, and repay existing bank debts.

SMR Jewels, an Ahmedabad-based heritage and antiquejewellery company, plans to raise Rs 63.7 crore. The IPO will run from May 26 to June 3 at a price band of Rs 125–128. The firm will list on June 8 and plans to use the funds for capital expenditure on constructing a new boutique jewellery studio, repayment of outstanding borrowings, and long-term working capital needs.

VAHH Chemicals, a manufacturer of industrial chemicals, plans to raise Rs 13.5 crore. The IPO will run from June 4 to June 8 at a fixed price of Rs 60. The firm will list on June 11 and plans to use the funds to meet corporate working capital requirements, execute debt repayments, and fund capital expenditure for a new manufacturing setup in Surat, Gujarat.

GenXAI Analytics, an AI-driven software and data tools provider, plans to raise Rs 54.8 crore. The IPO will run from June 5 to June 9 at a price band of Rs 110–116. The firm will list on June 12 and plans to use the proceeds to fund capital expenditure for developing new proprietary software platforms, meeting working capital requirements, and paying down debt.

UHM Vacation, a Mumbai-based travel and tourism aggregator, plans to raise Rs 36 crore. The IPO will run from June 4 to June 8 at a price band of Rs 157–166. The firm will list on June 11 and plans to use the proceeds to fund its marketing and promotional activities, meet corporate working capital requirements, and cover capital expenditure for technology upgrades.