By Swapnil Karkare“The America I loved is gone,” the author Stephen Marche wrote in the Guardian last month.

It's not just the writers who are feeling this way. Politicians, investors, students: everyone is re-evaluating the US. The Trump upheaval - Trump coin, the Qatar plane, everyday a circus - has made the world look at America differently. Trump's on-again, off-again, on-again tariffs have earned him the nickname TACO Trump - "Trump Always Chickens Out".

Asian investors hold $7.5 trillion in US investments, while Europe holds around $4.1 trillion. In the volatile Trump era, investors holding "too much in the US" are looking for ways to diversify their risk. And the Global South - a group of developing nations that include India, China, Brazil, Malaysia, Indonesia, Argentina, Thailand, etc - is becoming a serious contender for this money.

Together, this grouping contributes over half of global GDP. And the biggest countries are already toe to toe with the developed world. While the G7 (Canada, France, Germany, Italy, Japan, UK and US) accounts for 30% of the world’s GDP, the BRICS countries (led by Brazil, Russia, India, China, South Africa) also now match it at 30%.

Arvind Chari, the Chief Investment Officer at Q India, argues that if global investors reduce their US exposure by just 10%, that means $4 trillion of outflows from the US. And if only 5% of it moves to India, it would mean $200 billion of fresh flows, twice the current level. That’s almost 5% of India’s GDP.

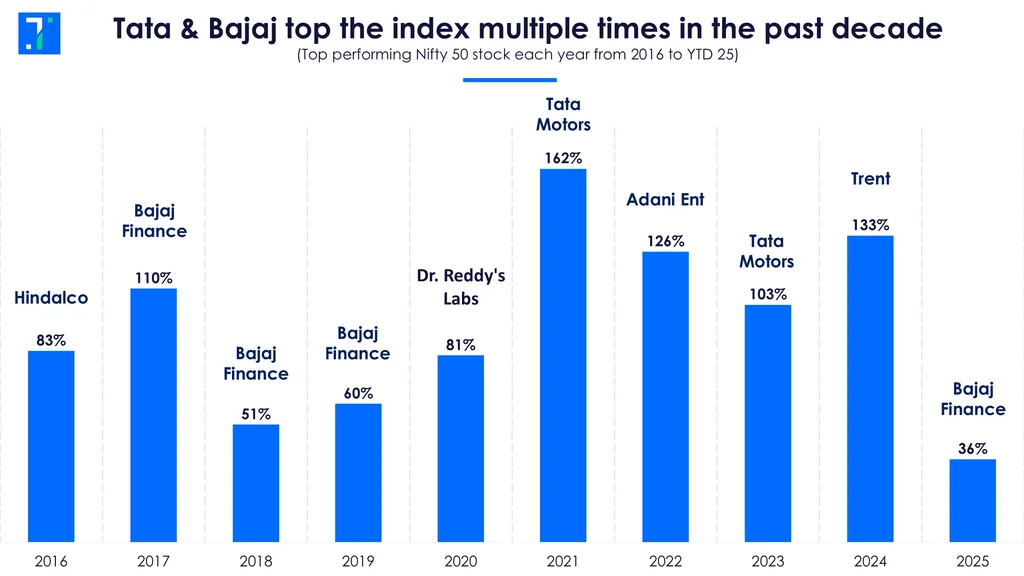

In this week's Analyticks,

- A global reset: A chance for India in global capital markets

- Screener: Companies with high debt and rising interest costs in FY25

Changing identities

For decades, the Global South has mainly been a source of raw materials. The world bought Brazil’s minerals, Indonesia’s rice, the Gulf’s oil, India’s skilled labour. But that is changing fast.

These countries aren’t just basic resource exporters anymore — they’re building supply chains around them, and exporting products.

Indonesia has stopped nickel exports and is now making lithium-ion batteries, aiding the EV supply chain. The clean energy shift tells a similar story. Brazil, India, and China now rank among the top seven globally in wind and solar capacity, according to Global Energy Monitor.

Rare earth minerals is another example. Economies like China, Vietnam, Brazil, Russia, and India hold most of the world’s deposits, but China dominates the processing. That’s a concern, and countries like Brazil are now stepping up processing to reduce dependence on Beijing.

Even the Gulf is thinking beyond oil, and investing in tourism and education. The UAE recently launched an AI-focused university, branded as the "Stanford of the Gulf", and startups like Presight AI are already expanding into places like Kazakhstan and Albania. They claim the Global South will ride the next AI wave.

Companies are shifting supply chains to the Global South

No example captures this moment better than Apple. In 2018, 47% of Apple’s suppliers were located in China. By 2023, that dropped to 34%. In contrast, shares of emerging Asian economies rose: Vietnam (+5 percentage points), Thailand (+3 ppt), India, Malaysia, and the Philippines (+2 ppt each).

“It’s a once-in-a-lifetime opportunity that no country wants to miss,” says economist Sonal Varma from Nomura.

Vietnam has seen a fourfold rise in Apple-linked companies over the past decade, while 7% of all iPhones are now manufactured in India. The shift goes beyond Apple. In 2023, the Global South as a whole attracted more FDI than advanced economies — $525 billion vs. $464 billion. These investments can spark a broader wave of industrial development across the Global South.

Communist, capitalist, autocratic, democratic? For now, ideologies don’t matter

Apple’s case highlights the complexity of today's supply chains. The world is no longer divided by rigid Cold War-style alliances. Today, both countries and companies are flexible in choosing their partners.

For instance, for most of the Global South, China is the largest trade partner, while the US is the dominant investment partner. This flexible approach allows countries to stay on the fence in their alliances.

BRICS has challenged the US-led global order, while bringing a diverse mix of countries together — from democracies to semi-autocracies, from countries with close Western ties to those under Western sanctions.

Analysts are betting on emerging markets

Investors are watching this unfold and rethinking their strategies. Arvind Chari points out that while the US makes up just 15% of global GDP, it commands over 50% of global market capitalisation. That kind of overconcentration raises red flags.

Christopher Wood of Jefferies recommends reallocating toward Asian assets in his latest report titled ‘The End of an Era’. Bank of America analysts are also bullish on emerging markets, citing a weaker US dollar, rising bond yields, and signs of China’s economic recovery.

“We could be at the start of a new rotation,” says Mohit Mirpuri of SGMC Capital — a view that’s increasingly echoed across global investment desks.

Despite recent volatility, India is a magnet for global capital flows

Among all emerging markets, India is drawing the most attention. Malcolm Dorson of Global X ETFs, Deutsche Bank, Bank of America and VanEck all view India as a long-term play.

However, absorbing large capital flows is challenging. Investor demand in India is booming, but the supply of new equity hasn’t kept pace. IPOs, FPOs, and QIPs have not matched post-pandemic investor enthusiasm, according to the RBI. That means a flood of capital chased a limited pool of listed securities, leading to elevated valuations, oversubscribed IPOs (even in the SME space), increased speculative behaviour, and intra-day trading losses for young investors.

Deepak Shenoy points out that many popular Indian services and products like PhonePe, Ola, Amazon, etc., are not listed in India.And among those that are listed, promoters still hold a dominant share, limiting the free float. That creates even more demand pressure on stocks, further inflating prices.

Untapped potential, in the past and now

Among India's great optimists is Nandan Nilekani. He is especially bullish about the future of Indian capital markets. He believes that by 2035, India could become the most preferred IPO destination globally. Many startups that were earlier registered abroad are now relocating their headquarters to India, eyeing listings. That shift could significantly broaden the universe of investable companies available to Indian and global investors alike.

For a change, there’s good reason to be optimistic.

When you compare India’s per capita GDP and per capita market capitalisation, the country falls below the trend line — meaning its market cap isn’t as high as it should be for its income level or conversely, its income is not as high as you would expect for its stock market value. Either way you look at it, there’s a gap.

But here’s an upside: India is expected to grow faster than most of its peers in the coming years. If that holds true, this gap could narrow, provided the gains come from structural improvements. That means more job creation, higher productivity, reduced poverty, and stronger capital markets with broader participation.

Now comes the hard part: Stock market fixes are needed

To tap this potential, especially with large-scale capital inflows expected, the capital market needs to be more welcoming and efficient. That starts with easing rules around listing, which are well-intentioned but often act as a barrier. Arvind Panagariya, former Vice Chairman of NITI Aayog, draws a sharp contrast between India’s SEBI and the US SEC. SEBI behaves like a strict parent, setting many rules that can discourage companies from listing. The SEC, by comparison, acts more like a watchful guardian, allowing companies to list as long as they are following the rules of the game.

This regulatory rigidity means many startups prefer listing in other global markets. But that’s changing.

Anand Rangarajan of Deutsche Bank believes Indian exchanges could see a wave of foreign listings — up to 44% of new listings — if FPI registration and KYC norms are relaxed. That would be a game-changer.

Screener: Companies with high debt and rising interest expenses in FY25

Auto stocks have high debt to equity and interest expenses in FY25

As companies release their FY25 results, we look at stocks with high debt and rising interest payments. This screener shows stocks with a debt-to-equity ratio greater than one (companies with debt than equity, indicating a higher reliance on borrowing to finance operations) and risinginterest expenses YoY in FY25.

The screener consists of stocks from the green & renewable energy, diversified services, electric utilities, realty, auto parts & equipment, and industrial machinery industries. Major stocks that show up in the screener are Adani Green Energy, Godrej Industries, Tata Communications, Signatureglobal (India), TVS Motor, JBM Auto, Kirloskar Oil Engines, and Grasim Industries.

Adani Green Energy has a high debt-to-total equity ratio of 6.4 in FY25. This green & renewable energy company’s interest expenses grew 9.7% YoY to Rs 5,492 crore during the year, with a relatively lower interest coverage ratio of 1.8. Adani Green has a total debt of Rs 78,069 crore as of FY25 on the back of its efforts to achieve a renewable energy capacity of 50 gigawatt (GW) by FY30. The company also plans a capex of Rs 31,000 crore in FY26 to add 5 GW capacity to its renewable energy portfolio.

Godrej Industries also features in the screener with a debt-to-equity ratio of 3.7 in FY25. This services company’s interest expenses grew 44.7% YoY to Rs 1,956.9 crore during the year, with an interest coverage ratio of 2.2. It has a total debt of Rs 37,851.3 crore as of FY25 on the back of its efforts to fund the acquisition of Raymond Consumer Care and to meet the increasing working capital requirements in the chemicals, agri-inputs and consumer products businesses.

You can find some popular screeners here.