By Swapnil KarkareIn 2002, I was in second grade, in possession of an unfortunate slicked-back hairstyle, and a big Sachin Tendulkar fan. That year, Sachin scored his 29th Test century, equalling Don Bradman’s record. The country celebrated it like a national festival. I remember watching the legend Michael Schumacher hand Sachin the keys to a bright red Ferrari 360 Modena at a special event.

But the story soon took on a familiar Indian flavour. Sachin immediately faced a challenge that Bradman never did: the customs duty on the Ferrari was about Rs. 1.5 crore, nearly twice the price of the car itself at the time. Tendulkar requested a waiver, and the government granted it, which in turn triggered a national controversy and even court scrutiny. Fiat, whose brand ambassador Sachin was at that time, finally paid the duty.

India’s trade policy has long been high-walled and protectionist, with steep tariffs and complex rules. But if the current trend holds up, the next sportsperson may not have to worry about a massive customs bill.

India is opening up its economy. It's slow, yes - that's the way we do things. But in the last couple of years, India signed trade deals with the EU, the UK, Oman, New Zealand, Brazil, Canada, the UAE, the US, and the European Free Trade Association (EFTA, which includes Switzerland, Norway, Iceland and Liechtenstein).

Economist Arvind Subramanian argues that if these agreements are fully implemented, India could move from being one of the world’s more protected economies to one of the more open ones.

What does all this openness mean for us? Some of the signals will be superficial: smaller duties for a Ferrari landing in India, not needing that Dubai trip to buy a cheaper iPhone.

While shopping abroad, you might also start spotting familiar Indian food, clothing and pharma brands on international shelves. The new trade deals commit to bringing Indian products to different countries, and making it easier for global brands to enter India.

Pharmaceuticals get an export boost

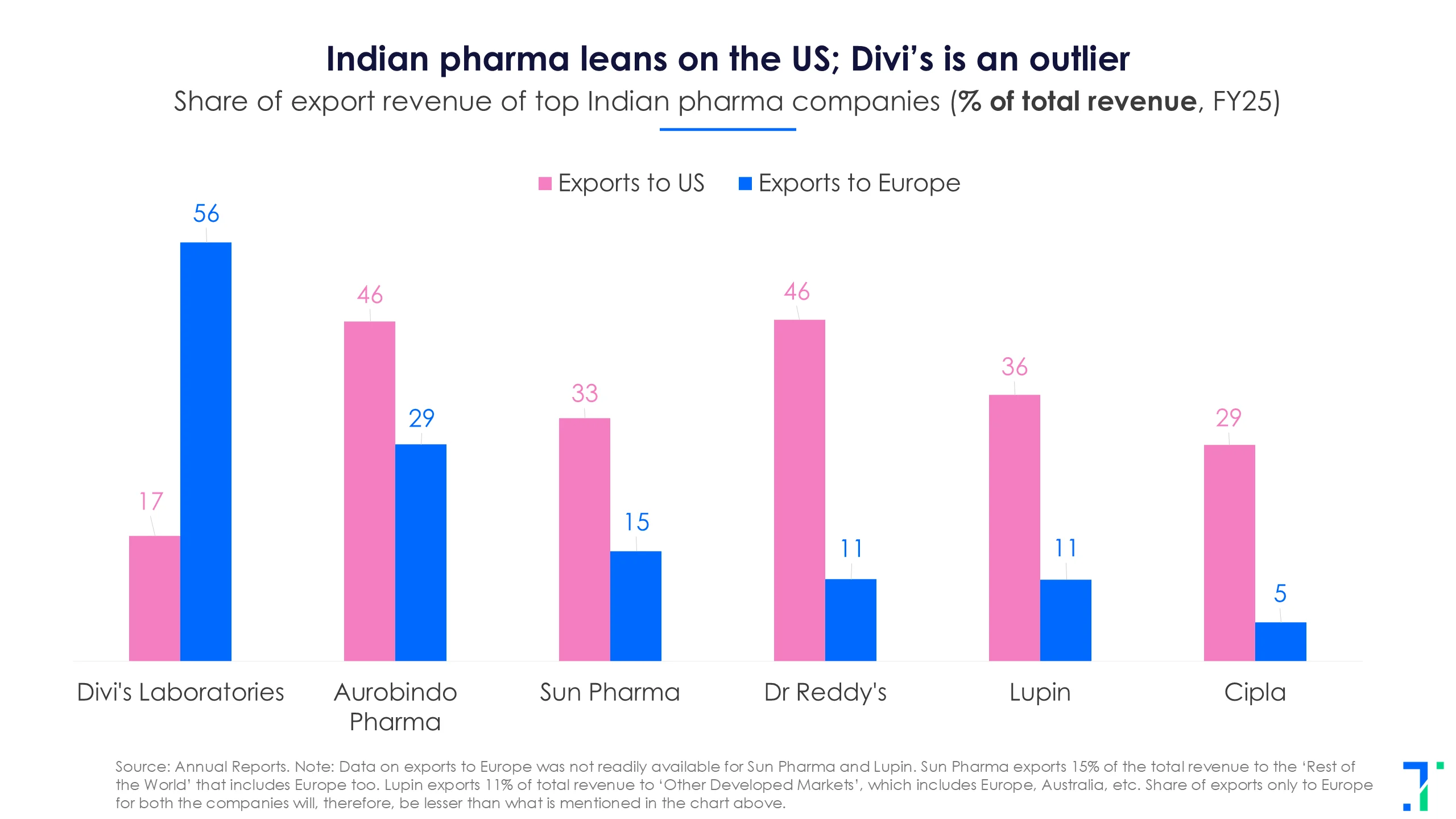

Exports of Indian medicines are set to rise rapidly, because of near-zero tariffs and faster approvals for Indian generics in the EU and UK deals. The UK’s£25 billion NHS procurement system and Europe’s massive generics market (where India already supplies 15–20% of medicines) are now more accessible.

Right now,India’s share in the EU’s total pharma imports is still less than 3%. Emkay Capitalnotes that easier approvals could help Indian companies file more applications in Europe, win more tenders and reduce their reliance on the US market.

New Zealand also recognises Ayurveda and traditional treatments in its agreement, while the EFTA deal removes the 7-15% tariffs on precision machinery used for drug manufacturing.

The only uncertainty is the US, which has become more protectionist itself, and where tariff relief depends on a Section 232 review on whether imported Indian medicines "pose a national security risk". One suspects that our 2002-era Indian bureaucrats would be very comfortable in Trump's US, with all its new customs tariffs, reviews and rules.

Companies likeAurobindo Pharma andDr Reddy’s earn close to half their revenue from the US, and are the most exposed if US policy turns restrictive. Meanwhile,Divi’s Laboratories already sells heavily into Europe, and stands to benefit from deals with the EU, UK and EFTA.

Time for Indian jewellers to shine

Jewellery exporters are also in a sweet spot. The US deal removes tariffs on gems and diamonds, which is a direct boost for Surat, the world’s diamond-cutting powerhouse. Kirit Bhansali, who heads the Gem & Jewellery Export Promotion Council, said that the pact with the US could help exporters win back ground at a time when shipments to the US have dropped by nearly 44%.

Companies like Goldiam International, which earns 90% of its revenue from the US, and Rajesh Exports,with up to 18%, are set to gain the most. Even retailers like Titan and Kalyan Jewellers are expanding globally, and will benefit from these deals. For instance, Titan doubled its overseas jewellery stores from 14 in 2023 to 27 by 2025. Kalyan Jewellersexpects its international store count to reach 49 by FY27 from 33 in FY23.

Competition with Bangladesh and Vietnam is rising in textiles

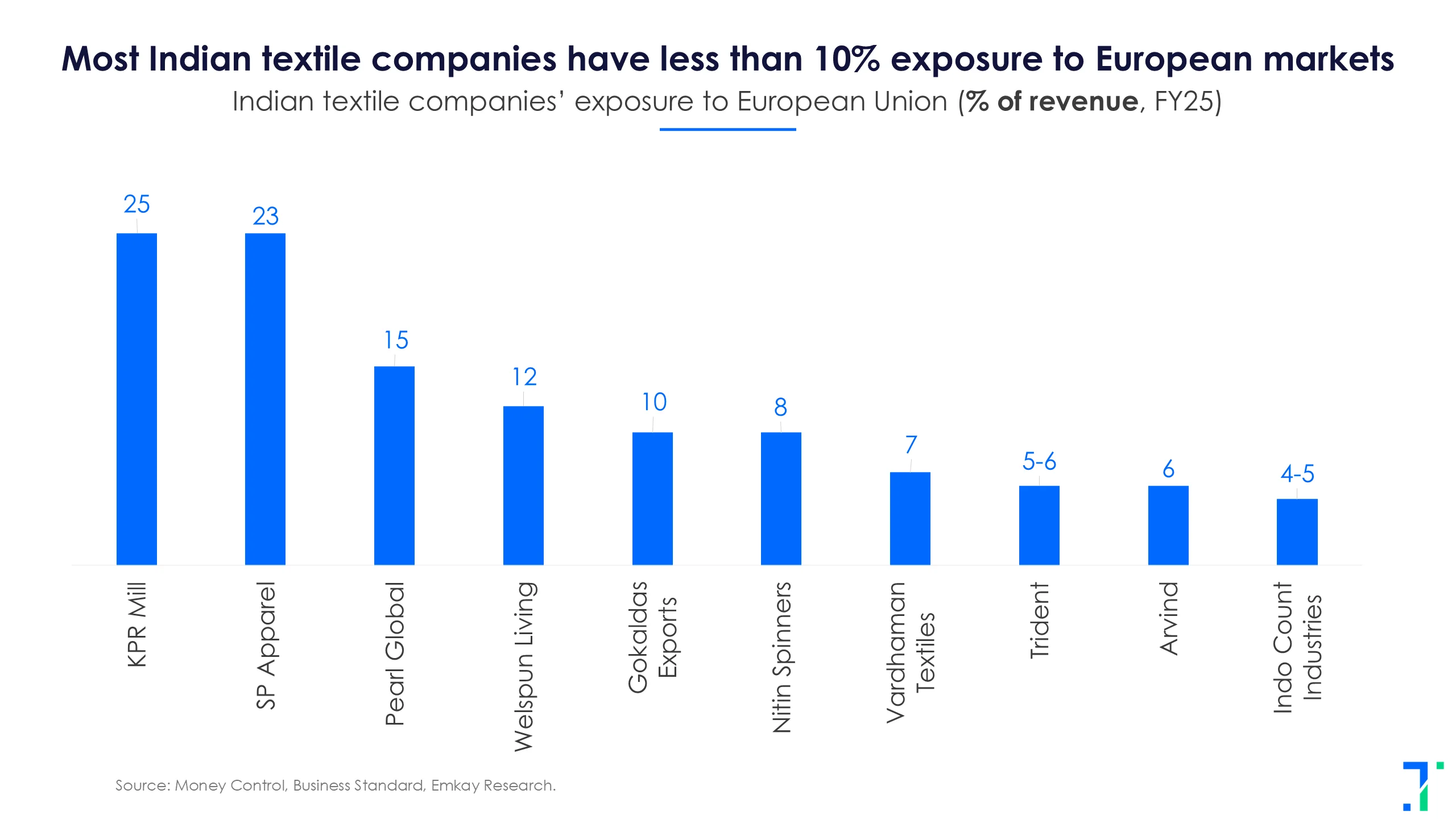

Textiles and apparel could see some of the biggest gains from tariff cuts. The UK and EU deals eliminate tariffs on almost all textile products, which is well-timed because Bangladesh will lose its duty-free access to Europe around 2029 as it graduates from “least-developed country” status. This gives India a chance to gain market share. The US is a different story, though. Tariffs remain at 18%, only slightly better than Vietnam (20%) and Bangladesh (19%).

This means Europe-focused Indian textile firms are set to benefit the most. Emkay Capital seesKPR Mill (~25% exposure to Europe) and S.P. Apparel as clear winners. In home textiles, Welspun Living, whose bedsheets are sold in Walmart and Target, earns about 10-12% of its revenue from Europe, a strong opportunity.

Auto components to see a smoother ride than car makers

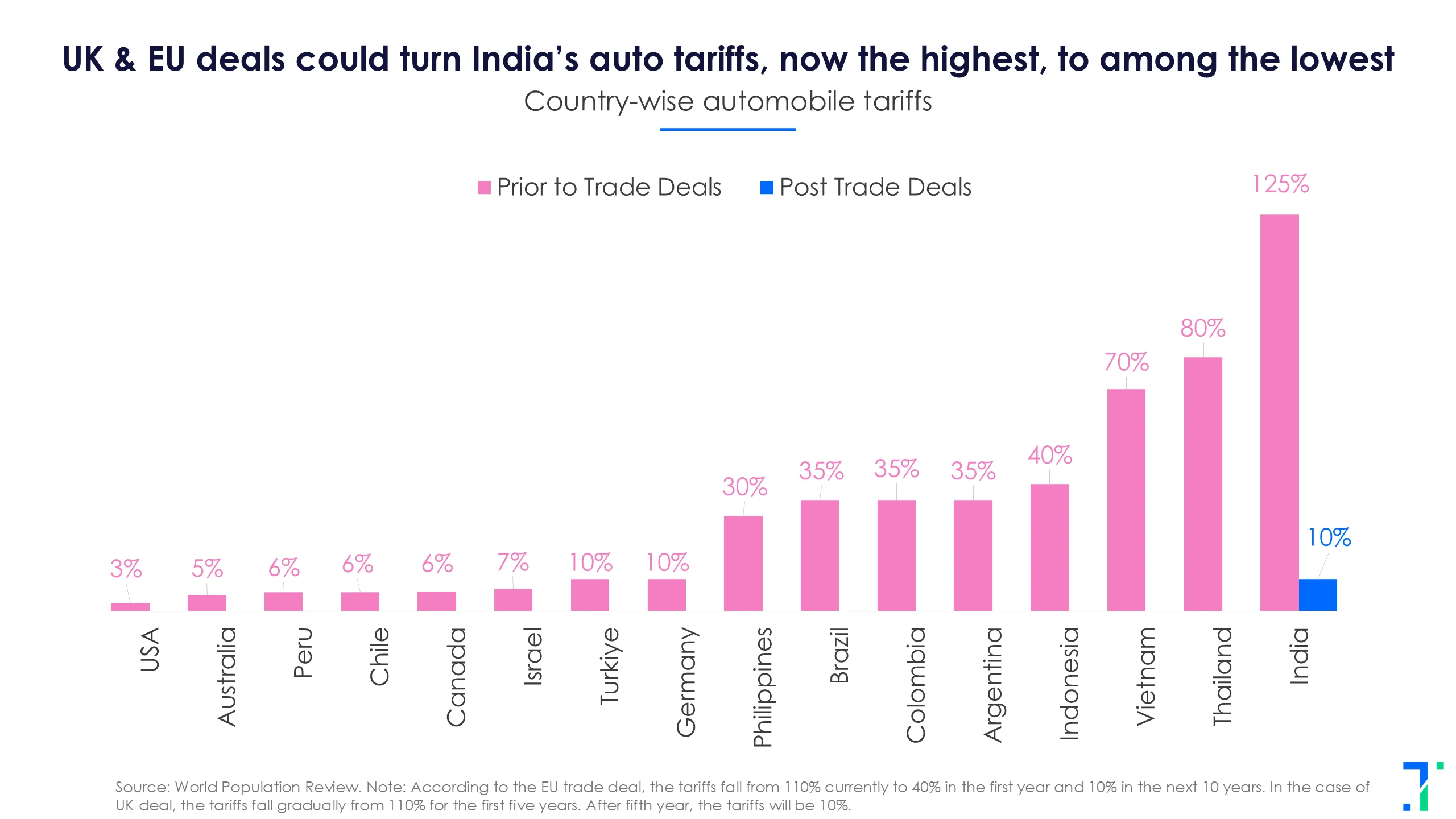

The automobile sector brings both opportunity and pressure. European cars will be cheaper to import into India soon, with tariffs going from 110% down to just 10% over ten years. There's a limit of 250,000 cars each year during this phase. The result will be more European cars on Indian roads, giving a tough battle to a long-protected sector: Indian car makers, especially in the mid-premium segment.

Auto parts makers however, are in for a good time. The EU deal makes it easier for Indian suppliers to plug into European supply chains, especially for EV parts.

For the US market, Section 232 tariffs haven’t gone away. But India does get a quota: a set amount of auto parts can head to the US with lower duties, so there’s still some relief for exporters.

Auto-component exporters with well-established export supply chains are the winners. Companies such as Sona BLW, Bharat Forge, Samvardhana Motherson, CIE Automotive,Endurance Technologies, and Precision Camshafts, many of which already earn 20-50% of their revenue from North America and Europe, should benefit from this shift.

IT Services to benefit from the easing of visa policies

Services have also got wins in these deals. Indian professionals in the UK can now avoid social security payments for up to three years, reducing IT firms' costs by around 20%. By locking in commitments across 144 service sectors, including IT, R&D and other professional services, the EU deal opens doors to the $300 billion IT market.

It also pushes both sides to invest more in tech and to work together on AI, semiconductors and clean tech research and makes it easier for skilled professionals such as IT consultants and software engineers to temporarily work in Europe.

Countries like New Zealand and Oman are also easing their visa policies. This comes at a good time for major Indian IT exporters such as TCS, Infosys, Wipro and HCL Technologies, especially after the recent hikes in US visa fees.

However, Phil Fersht of HFS Research notes that the US deal is mostly symbolic for this sector, since IT revenues depend on visas and tech budgets, not tariffs. US tech companies, says Pareekh Jain of EIIRTrend, are likely to benefit most by boosting cloud and AI sales in India through local partners.

The agricultural sector is set to crack open

Agriculture is always the tricky part of any trade deal, but this time India has opened up in a selective way. The UK has removed shrimp tariffs, unlocking a $5billion market. Switzerland has cut duties on multiple food preparations, and Norway now allows dutyfree entry for processed vegetables, rice and fruits. The Oman agreement simplifies Halal certification by allowing mutual recognition. But the politically sensitive dairyindustry stayed out of all agreements.

Kriti Khurana of BITS Pilani and former agriculture secretary Siraj Hussain point out that the real test for farm trade isn’t tariff cuts but whether these deals help India grow its agricultural surplus. And on that front, they believe the EU might have the biggest upside, especially for marine products, tea, coffee and spices.

Seafood exporters such as Apex Frozen Foods and Avanti Feeds are among the clearest winners from these deals. They earn about 35–40% and 15-20% of their revenue from Europe, respectively.

Of all the agreements, the EU deal may turn out to be the most practical and impactful. It offers clearer tariff cuts and fewer political surprises compared to the US framework, where outcomes still depend on legal procedures, the Section 232 investigation, and, frankly, Trump’s mood swings.

Free trade agreements do not of course, automatically translate into export growth. The hard part is simplifying tariffs and meeting export standards in these sectors, particularly for the EU which is famously exacting in its standards. As economist Shoumitro Chatterjee notes, these are areas where India has often struggled.

If India pulls that off, we may be in for an unprecedented export boom.