When a company repurchases its own shares, it returns surplus cash rather than investing it elsewhere. This can signal confidence in the business, but it can also reflect limited near-term expansion opportunities. In India, buybacks remain uncommon and are usually limited to a few large companies each year.

In contrast, US companies routinely use buybacks as a capital-return tool. Companies repurchased over $1 trillion of shares in 2025, as investors expect regular cash returns and firms use buybacks to support earnings per share and stock prices through flexible payouts.

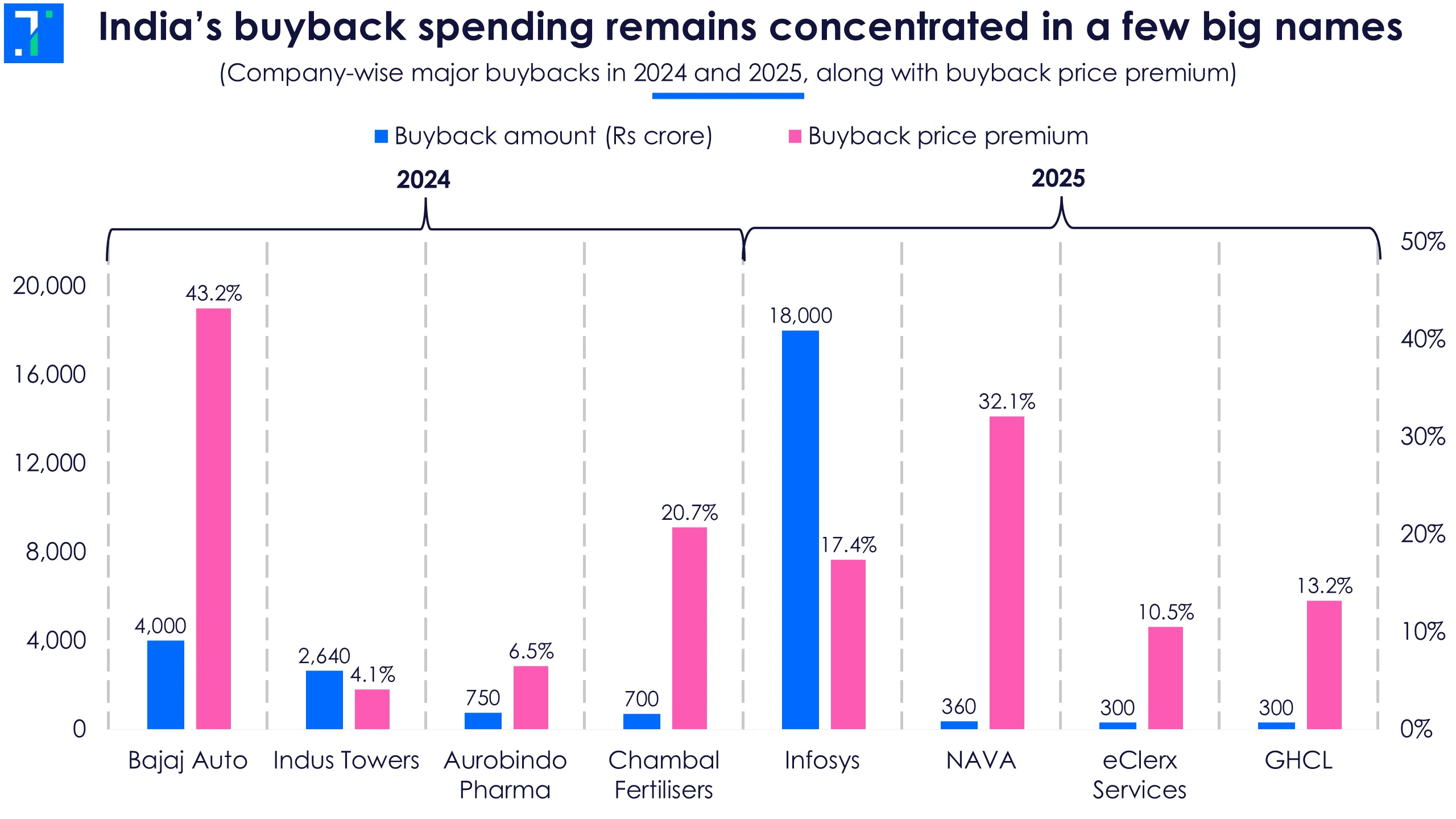

In 2024, Bajaj Auto executed a Rs 4,000-crore buyback, the largest of the year. In 2025, Infosys made headlines with a Rs 18,000 crore buyback. Overall, 15 companies repurchased shares worth Rs 19,749 crore in 2025, with Infosys accounting for the majority.

After the Union Budget 2024, the buyback tax shifted from companies to investors. So when you sold your shares back to the company, the money you received was taxed like a dividend, based on your income tax bracket. For large investors (promoters) in the highest tax bracket, this meant paying around 39% or more in tax. It made buybacks less appealing.

New changes in 2026-27

The Union Budget 2026–27 has changed this. Now, money from a buyback is taxed as capital gains rather than dividend income. Replacing the dividend-based system introduced in 2024 makes the taxation fairer and more transparent. It encourages investors and companies to pursue buybacks for business reasons without being heavily penalized by high taxes.

Amit Gupta, Partner at Saraf and Partners, explained, “Earlier rules taxed the entire buyback amount as dividend income to stop big investors from misusing it, but it also hurt regular investors by taxing their invested capital.”

He noted that while the tax is still paid by investors, “treating buybacks as capital gains allows investors to deduct what they originally paid for the shares”.

In this edition of Chart of the Week, we examine how capital-gains taxation of buybacks affects promoters and public shareholders differently, and why buybacks are still popular as a cash-return tool.

How buybacks were taxed, and why it mattered

Under the 2024–25 regime, buyback proceeds were taxed as dividends in the hands of shareholders at their income-tax slab rates, often exceeding 30%. Since the tax applied to the full amount received, investors effectively paid tax even on the return of their own original capital.

Many investors faced difficulties because they could not offset the cost of their shares against this dividend tax. Instead, the system recorded a “capital loss” that investors could carry forward only to offset future capital gains, not the immediate buyback tax.

This marked a sharp break from the pre-2024 system, in which companies had paid a flat ~23% tax and shareholders received buyback proceeds tax-free. While the 2024 change aimed to tax promoters at their personal slab rates, it inadvertently turned buybacks into one of the most heavily taxed forms of capital return globally.

Although the 2024 structure succeeded in closing a perceived “tax loophole”, it also distorted payout decisions by making buybacks more expensive for major shareholders than straightforward market sales.

What the new tax framework changes

Under the 2026–27 Budget, the government no longer treats share buybacks as dividends. From April 1, 2026, investors will not face the earlier 10% tax deduction at source on buybacks. This change puts more cash directly in the hands of resident investors and makes buybacks simpler to understand and receive.

The tax now applies only to the actual profit—the difference between the buyback price and what the investor paid for the shares. Long-term gains face a 12.5% tax (with an annual exemption of up to Rs 1.25 lakh), while short-term gains are taxed at 20%. These rates replace the earlier slab-based taxes that often crossed 30%. Retail investors benefit because the tax no longer applies to money that simply returns their original investment.

For promoters, the change restores balance while closing tax loopholes. Any shareholder with a 10% or higher stake is treated as a promoter and pays an extra levy. This lifts the effective tax to about 22% for corporate promoters and 30% for individuals and NRIs, keeping their tax burden close to earlier dividend levels.

Kunal Savani, Partner at Cyril Amarchand Mangaldas, noted, “While the shift to capital gains is a relief, promoters may still pay a higher overall tax than retail investors due to surcharges, resulting in a more layered tax outcome for controlling shareholders.”

Why buybacks will still remain relevant

By removing the dividend-tax “penalty”, the new regime restores the economic logic of buybacks. Companies can continue to use buybacks effectively when their shares trade below intrinsic value. By reducing the number of outstanding shares, repurchases lift earnings per share and improve returns for remaining shareholders.

Plus, companies no longer face the “double-whammy” of taxing capital returns as income. Firms with surplus cash, strong balance sheets, and confidence in their valuations will continue to use buybacks to optimize capital structures.

Recent trends support this. Software and IT services companies accounted for about 40% of buyback activity in 2025. Their cash-heavy balance sheets, low reinvestment needs, and flexible payout preferences make buybacks a natural choice even under the new tax rules.

Amit Chandra, vice-president at HDFC Securities, said, “IT services companies may increasingly opt for buybacks, as they now benefit not only retail investors but also corporate promoters, who can now offset their cost of investment.”

The tax reset improves the quality of capital-return decisions. Dividends continue to provide steady payouts, while buybacks now serve their intended role as tools for capital optimization and valuation signaling.