For many investors, the past year raised an uncomfortable question: was taking the extra risk in the stock market worth it?

After months of weak returns and volatility, a safe fixed deposit has been looking a lot more attractive.

The past week has brought relief and some green into market returns, now that (after several false starts and bombings) a US Iran deal is finally on the table.

We are in an era where winning the social media narrative is necessary even for large nation states. So a modern war cannot have any losers. As The Wall Street Journal’s Benoit Faucon put it, “Both sides have framed the ceasefire as a victory.”

The deal has been celebrated by Indian markets, and the Nifty is up 3.4% in the past week. But a few good days does not answer the bigger question: if you had invested in India’s largest companies over the last 1, 3, or 5 years, would you have done better than someone who locked their money in an FD?

Within the market, why did some stocks multiply investor wealth while others failed to clear even the FD benchmark?

The answer reveals why this has become a stock picker’s market, where specific bets matter more than just staying invested.

Let’s dive in.

The time advantage: beating fixed deposit returns

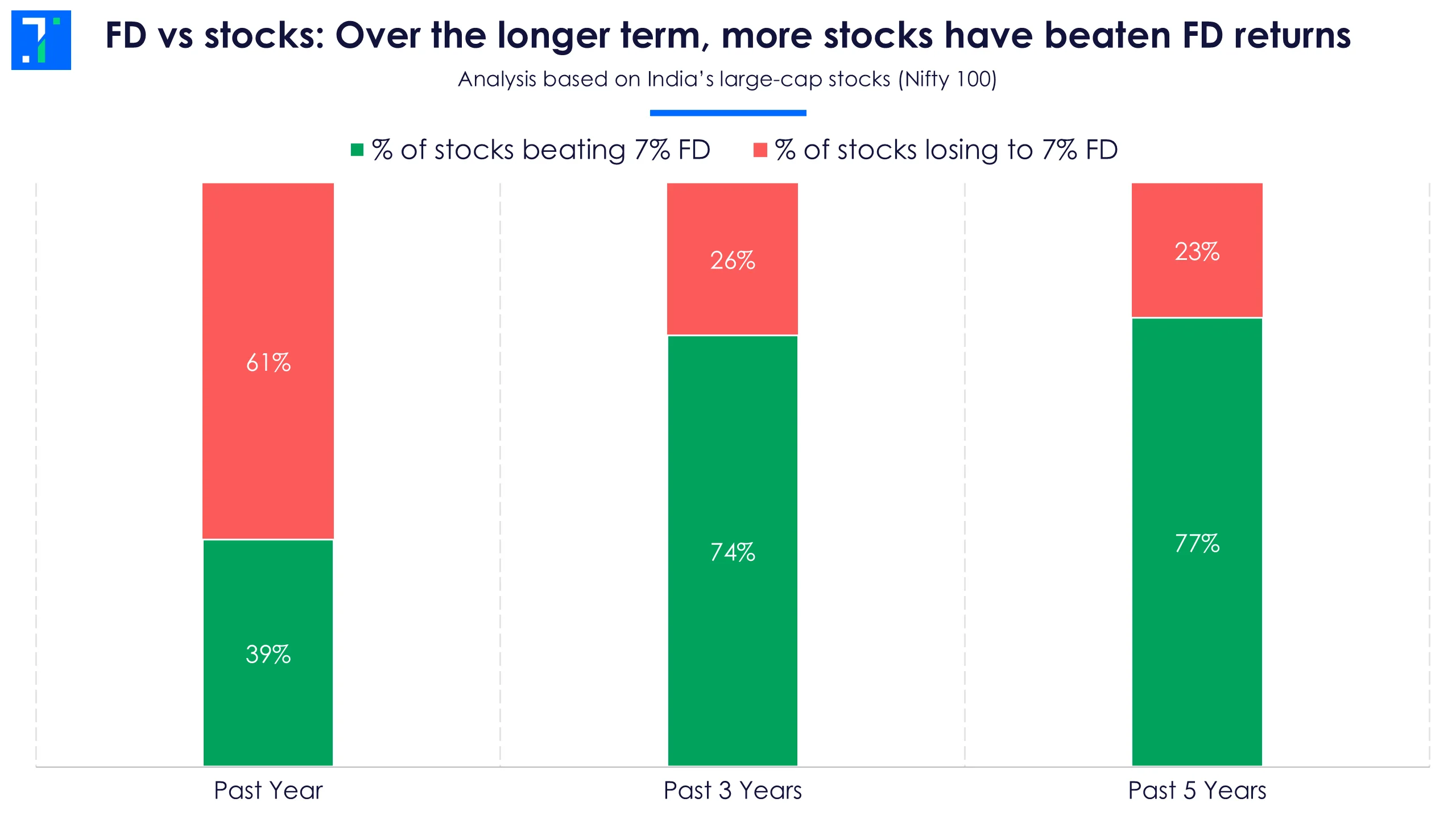

Despite the recent bounce, India’s large-cap benchmark, the Nifty 100, has offered investors little to celebrate over the past year, slipping over 1%.

Over these 12 months, only 39% of its constituents managed to outperform a 7% FD return through price gains alone (excluding dividends).

But stretch your horizon to three or five years, and the success rate jumps to 74% and 77%, respectively. It is worth noting that the Nifty 100 index is rebalanced twice a year, weeding out the weaker players over time, but the broader trend holds up: patience pays off.

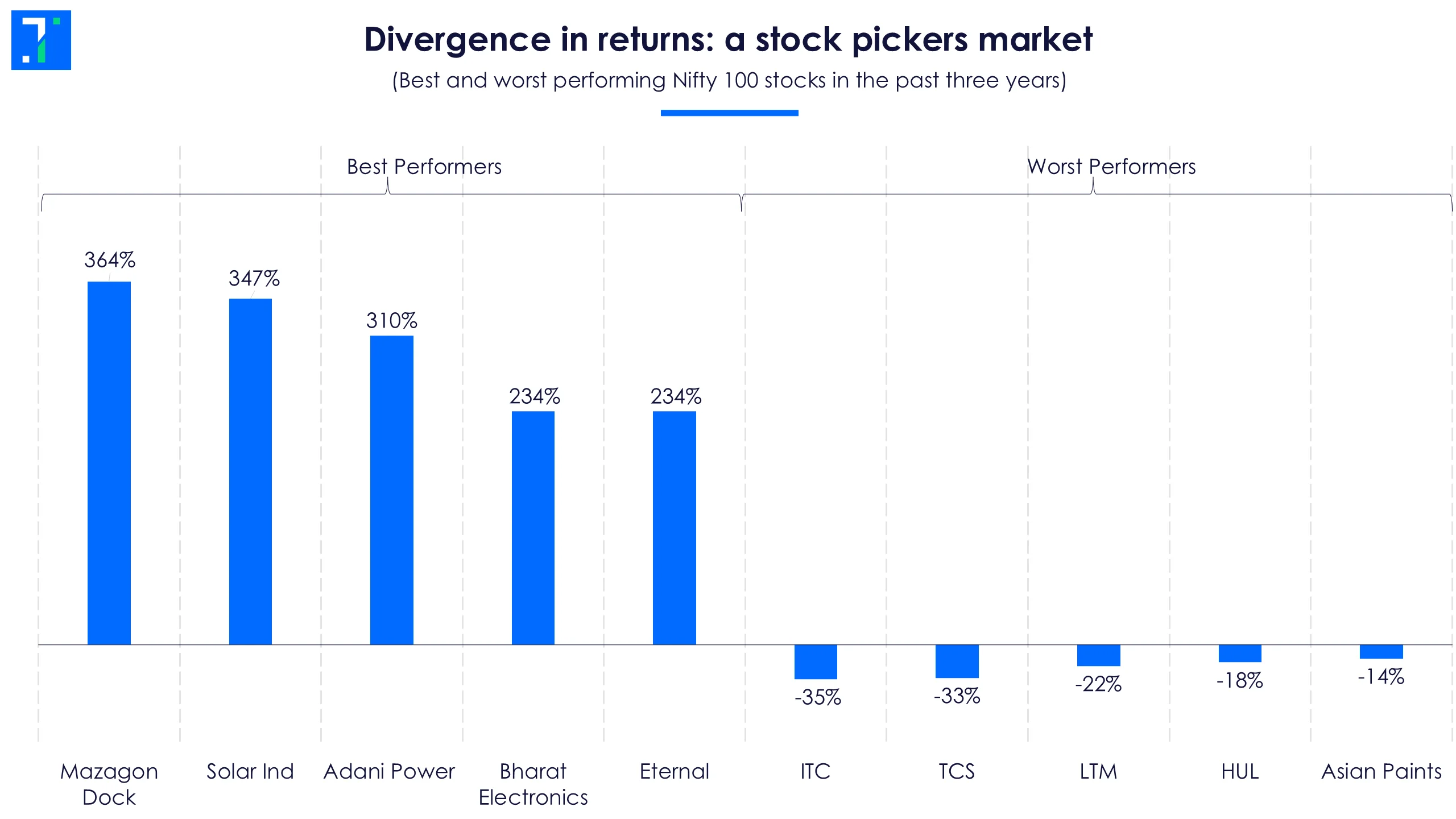

The three-year data also shows how uneven returns can be. Among the top 100 stocks, 30 became multibaggers, 54 generated positive returns of up to 100%, while 16 lost investor money.

So time is an advantage, but not a guarantee. Even over longer periods, a quarter of India’s biggest companies failed to beat a simple FD return. The real wealth creation came from identifying the businesses that pulled ahead of the pack.

What separates these winners from the laggards? Two patterns emerge.

The capex premium: the stock market rewards builders

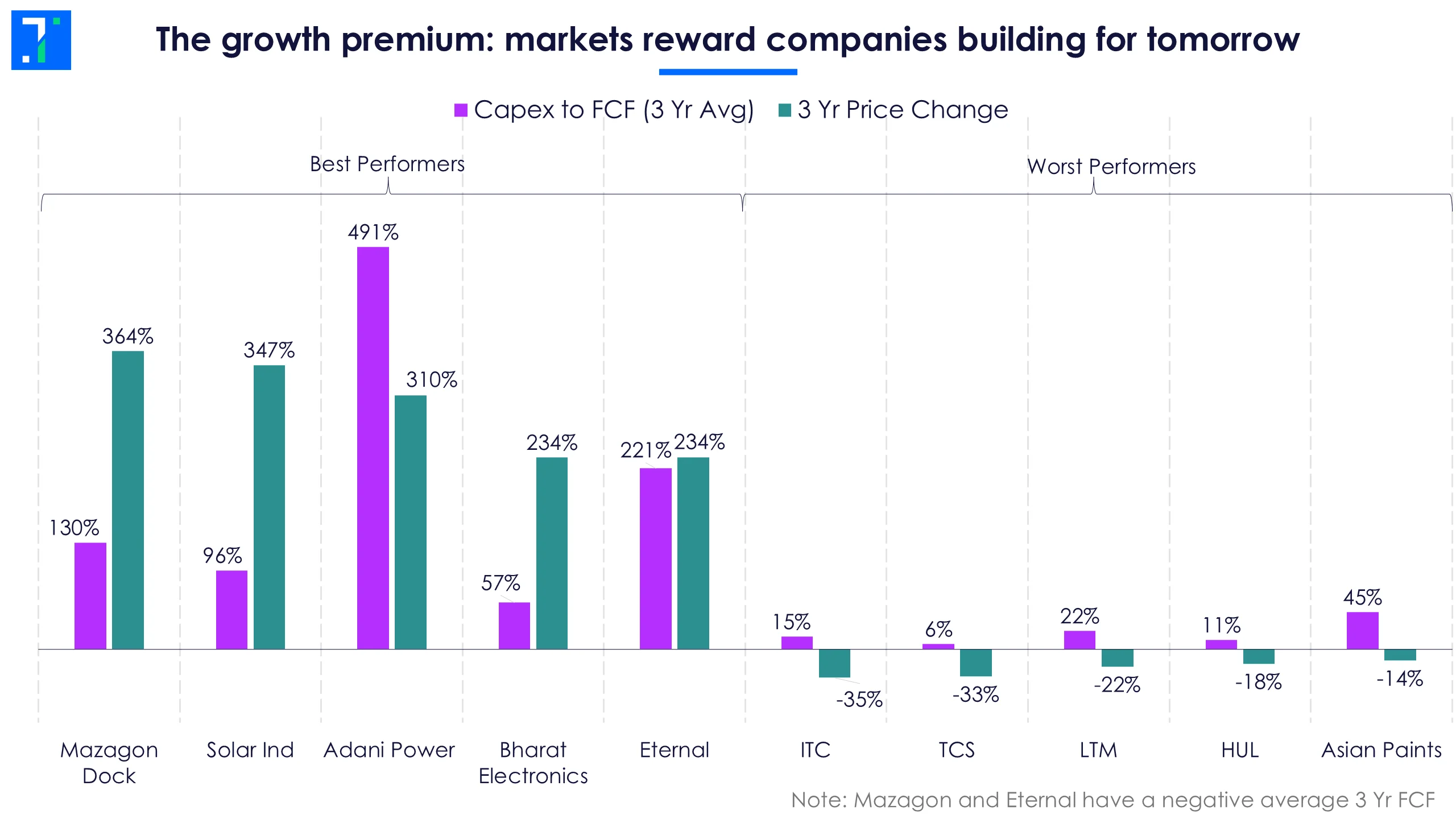

The first pattern is reinvestment. Companies that put more money back into expanding their businesses often pulled ahead. We measured this through the ratio of capital expenditure to free cash flow (FCF) over the past three years.

Overall, corporate India has held back on investment. While India's listed company profits are nearing a record 6% of GDP, their capital expenditure has remained mostly unchanged over the years at around 3.6–3.7% of GDP.

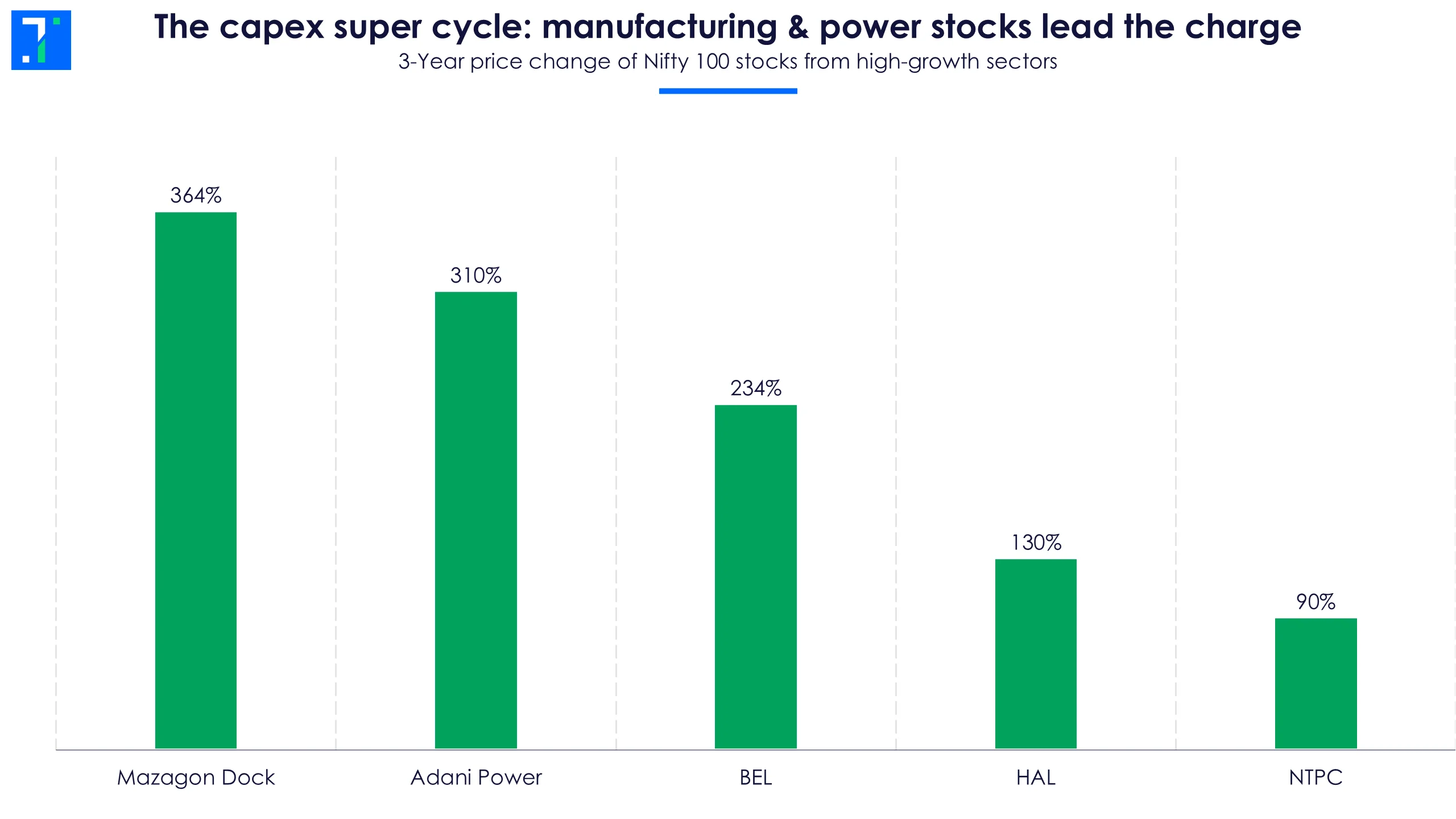

The market however, rewarded businesses that are reinvesting today’s cash flows to create tomorrow’s growth engines. Two of the strongest performers in returns, Mazagon Dock Shipbuilders and Eternal, lead this trend, with investors backing aggressive expansion plans even as heavy spending pushed their free cash flow into negative territory.

Companies that failed to deploy capital into new growth opportunities have seen their stock prices stagnate. While traditional capex is less relevant for asset-light IT companies, the broad takeaway holds: the market rewarded companies building for the future in India's high growth economy.

Asian Paints is the exception here, with its underperformance driven more by margin pressure from expensive crude oil and intense competition, rather than underinvestment.

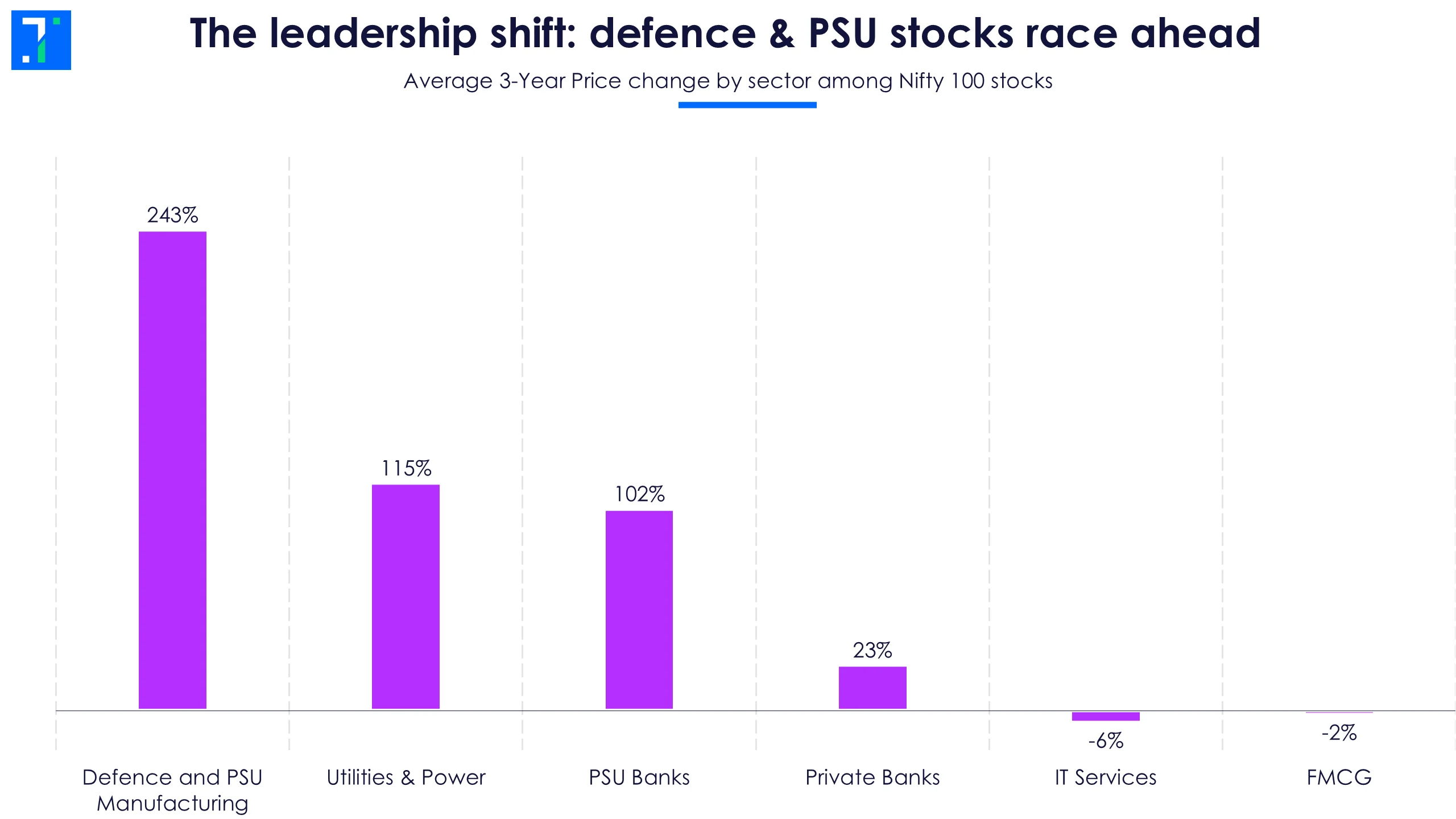

The great rotation: changing sector leadership

The second driver behind the winners and losers is sector rotation. Over the past three years, market leadership has shifted away from traditional favourites like IT and FMCG towards sectors benefiting from India’s infrastructure and manufacturing push.

India's economy is changing fast as it grows, and investor interest has moved towards the new stars: defence, PSU manufacturing, utilities, power, and PSU banks. These companies have delivered stronger earnings growth, supported by government spending, a revival in capex, rising power demand, and healthier bank balance sheets.

Pradeep Gupta, Co-founder of Anand Rathi Group, says that this shift is backed by India’s ongoing investment cycle. “The first and most compelling bet is domestic cyclicals linked to capex and manufacturing. India’s growth continues to be domestically driven, supported by sustained public capital expenditure in infrastructure, defence, railways, energy transition, and logistics,” he said.

Stocks like Mazagon, Bharat Electronics, Adani Power, and Hindustan Aeronautics are capitalising on expanding order books and rising power demand.

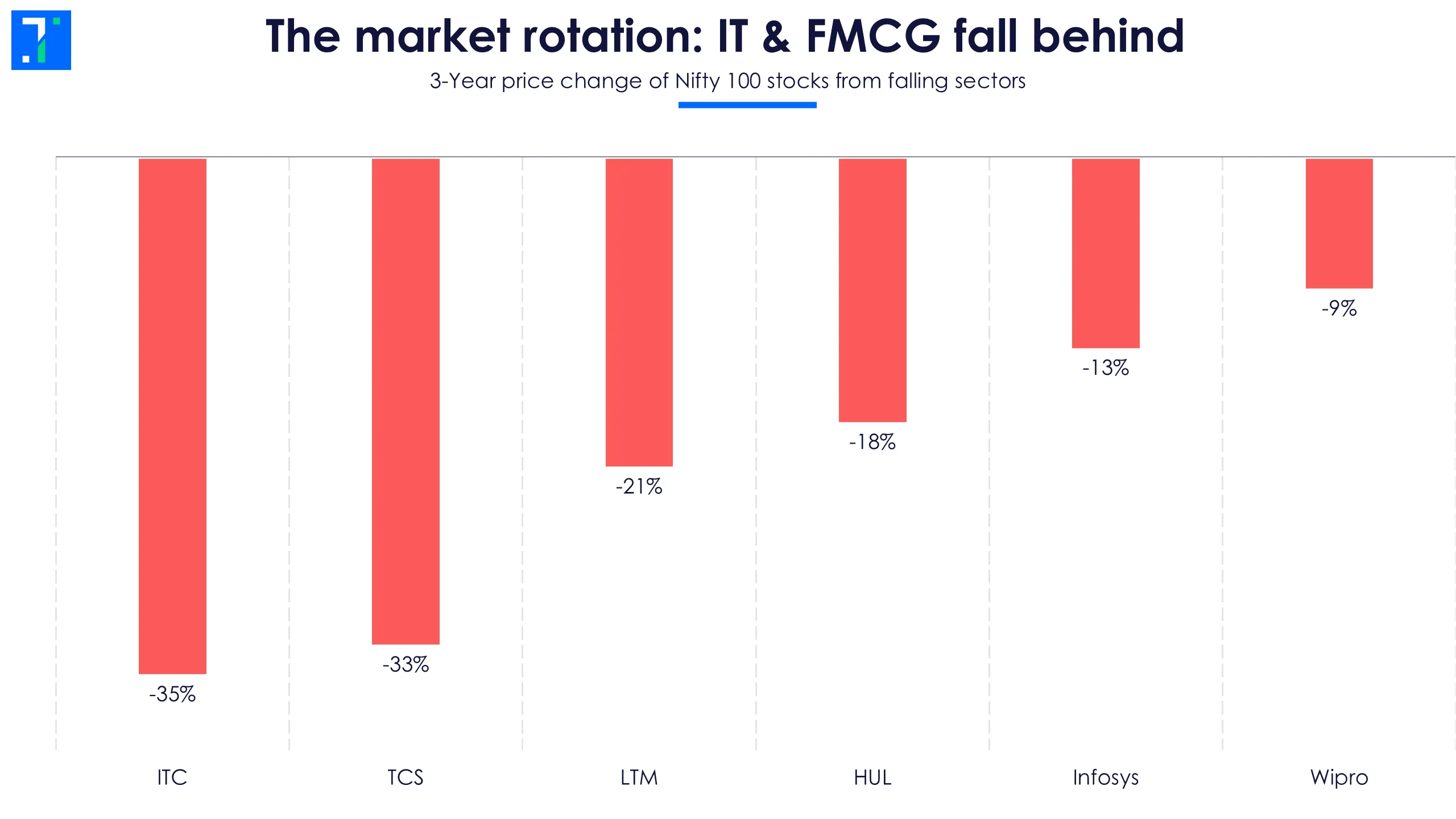

Meanwhile, the stock market royalty of the previous decade has been left out.

IT stocks took a hit as global clients in the US and Europe tightened tech budgets, delayed projects and cut discretionary spending. Adding to the friction is the uncertainty around AI and what it means for traditional IT pricing power. Giants like TCS, Infosys, and Wipro have struggled to find their footing in the current landscape.

FMCG companies face a different challenge: expectations and volatile weather patterns. Stocks like Hindustan Unilever continue to trade at premium valuations, but earnings growth has not kept pace. Weak rural demand and inflation-hit consumers have made it harder to justify their multiples.

The lesson from the past three years is that a rising market no longer lifts everyone. Creating wealth now requires being selective, looking beyond index exposure and identifying where the growth, investment, and earnings momentum actually is.