By Suhani Adilabadkar

The banking bell-weather HDFC Bank reported stable Q4FY21 numbers on Saturday last week. The closely watched asset quality figure came out stable, reassuring investors and analysts alike. Although sequentially its net profit declined 18% in March quarter FY21 and corporate advances exhibited fatigue, other significant parameters - net revenues, CASA, other income, NIMs were on a strong footing. Management commentary was also robust dispelling fears of economic deceleration for now, and indicated the bank’s belief that they will see solid robust growth in FY22.

Quick Takes:

-

GNPA ratio at 1.32% in Q4 FY21 vs pro forma GNPA ratio of 1.38% in Q3 FY21. Net NPA ratio stood at 0.40% with no change sequentially on pro forma basis.

-

During Q4 FY21, new salary accounts acquired were 34% higher than the comparable period last year. HDFC Bank is the largest player in the corporate salary space.

-

The corporate loan book has grown above 20% every quarter in FY21 and reported growth of 21.7% YoY and 5.2% sequentially.

-

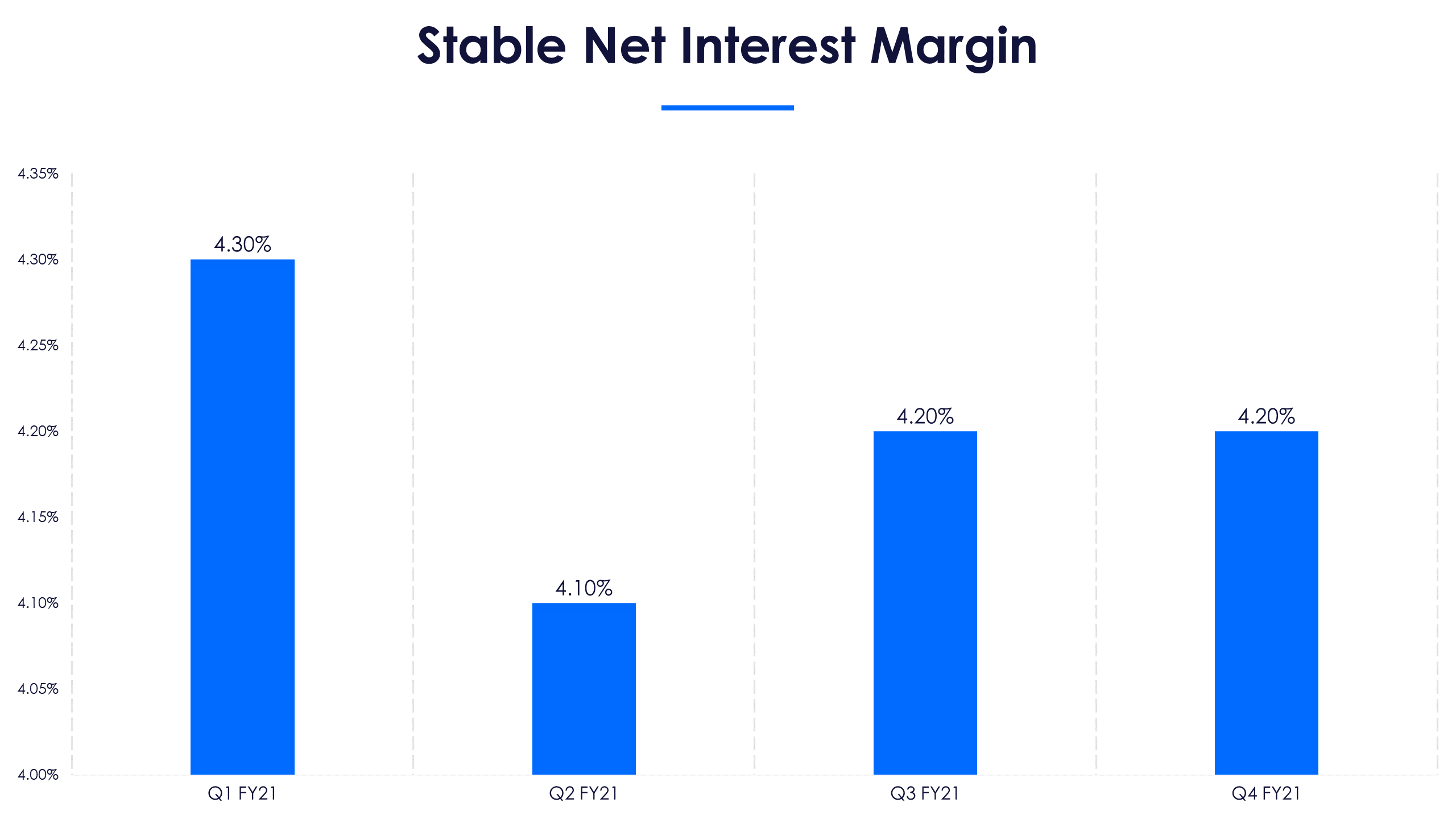

The bank has maintained NIMs within the range of 4.1-4.5% for the past 10 years.

Asset quality remains stable in Q4FY21

The March 2021 quarter saw the usual double-digit growth trajectory for HDFC Bank. NII (net interest income) for the quarter ended March 31st, FY21 came out at Rs 17,120 crore compared to Rs 15,204, a year ago, rising 12.6% YoY. NIM (net interest margin) was stable at 4.2% with no change sequentially and just a 10 bps YoY fall.

The bank managed to keep its quarterly net profit or PAT growth at 18% YoY for three consecutive quarters now. In Q4FY21, its PAT fell 18% to Rs 8,186 crore sequentially due to higher provisions.

The bank managed to keep its quarterly net profit or PAT growth at 18% YoY for three consecutive quarters now. In Q4FY21, its PAT fell 18% to Rs 8,186 crore sequentially due to higher provisions.

Provisions increased to Rs 4,694 crore in the March 2021 quarter, rising 24% YoY. Total provisions (comprising specific, floating, contingent and general provisions) were 153% of the gross non-performing loans as on March 31, 2021. Asset quality was stable with GNPA ratio coming out at 1.32%, rising 6 bps YoY while net NPAs increased 4 bps to 0.40% in Q4 FY21. Other income for the bank stood at Rs 7,594 crore, constituting 31% of net revenues and rising 26% YoY.

Total deposits as of March 31, 2021 were Rs 13.35 lakh crore, an increase of 16.3% YoY while advances rose 14%. CASA deposits comprised 46% of total deposits as of March 31, 2021. During FY21, the bank added 354 branches with 123 of them in the March 2021 quarter.

Total deposits as of March 31, 2021 were Rs 13.35 lakh crore, an increase of 16.3% YoY while advances rose 14%. CASA deposits comprised 46% of total deposits as of March 31, 2021. During FY21, the bank added 354 branches with 123 of them in the March 2021 quarter.

A pandemic proof bank?

A pandemic proof bank?

HDFC Bank tightened its sails even before the Covid-19 thunderstorm hit Indian shores. Dealing with a slowdown 18-20 months prior to Covid, the bank reinforced its credit standards, improved the underwriting machinery and undertook policy filtering to lower delinquency and strengthen the robustness of its loan book. For instance, wholesale or corporate loan book is rigorously measured against an internal rating scale (1-10, 1 is the safest), which is reaping higher benefits post Covid.

With retail revenues on a decline due to the cautious stance adopted by customers going slow on consumption and high on savings, the wholesale/corporate book came to HDFC bank’s rescue. Its top notch credit standards ensured high quality corporate book and the bank focussed its energies on PSUs, highly rated private companies and MNCs operating in sectors like consumer, infrastructure, energy, discretionary etc.

The corporate loan book has grown at 20% in all quarters in FY21. In Q4 FY21, corporate loan book growth was 21.7%% YoY and 5.2% sequentially. The wholesale SME book has crossed Rs. 2 lakh crore in advances and now constitutes one-fifth of total advances. The bank has acquired about 2,500 new customers during the quarter, a 60% increase YoY. Rahul Shukla, Group Head-Corporate Banking & Business Banking, said that the SME segment earnings are 2.2 times of equivalent lending to large corporates.

While the wholesale lending business held steady, throughout the year, retail, despite tepid growth, is on the path to recovery. Although retail advances continued to grow in single digits, with 6.8% YoY and 4.5% sequential growth in Q4FY21, the management clarified that this business is getting back to pre-pandemic levels. Jimmy Tata, Chief Risk Officer at HDFC Bank, said that the bank is witnessing a healthy growth trend in auto, housing, pharmaceutical, chemical and SME retail segments. He further added that even in the first two weeks of April, retail growth is looking robust compared to 2019 levels.

While the wholesale lending business held steady, throughout the year, retail, despite tepid growth, is on the path to recovery. Although retail advances continued to grow in single digits, with 6.8% YoY and 4.5% sequential growth in Q4FY21, the management clarified that this business is getting back to pre-pandemic levels. Jimmy Tata, Chief Risk Officer at HDFC Bank, said that the bank is witnessing a healthy growth trend in auto, housing, pharmaceutical, chemical and SME retail segments. He further added that even in the first two weeks of April, retail growth is looking robust compared to 2019 levels.

An asset quality benchmark

HDFC Bank has been an asset quality benchmark for the banking industry as a whole. The Supreme Court on 3rd September 2020, had directed banks that accounts not declared NPA till August 31st, 2020 should not be declared as NPA until further orders. The bank, as a matter of prudence using its analytical models, provided for corresponding contingent provisions and estimated potential NPAs (or pro forma basis) for Q2 and Q3 FY21. As the Supreme Court gave its final order on March 23 2021, RBI issued directives to banks to follow its instructions and IRAC norms for asset classification. Due to this, the March 2021 quarter was significant in assessing the asset quality strength of Indian banking sector. HDFC Bank has come out in flying colours.

Though at the first look, HDFC Bank’s Gross NPAs (GNPAs) look elevated compared to December 2020 quarter (0.81%), but at 1.32%, it is lower than proforma GNPAs of Q3 and Q2 FY21 at 1.38% and 1.37%, respectively. Net NPA ratio was at 0.4% of net advances, is also at the same level on a pro forma basis as in the December 2020 quarter. In the same period of the previous year, it was at 0.36%. In addition to stable asset quality and growing loan book amidst the pandemic, the operating efficiency of the Bank is also high with CASA ratio at 46% and NIMs at 4.2%. The bank has maintained NIMs within the range of 4.1-4.5% for the past 10 years.

Robust management commentary

And lastly, on the second wave’s impact on Indian economy. Will it be worse than the first wave? The management said that although the situation is grave across the country, the impact on the financial system may not be as severe as the first Covid-19 wave, noting that the lockdowns imposed in India were sporadic and localized. Manufacturing, logistics and transformation are not facing disruptions and government restrictions are more benign compared to stringent lockdowns imposed last year. And in case the situation grows worse, the banking sector is expecting a second round of stimulus from the government and RBI.

The management on its part is optimistic of logging in robust growth in FY22, similar to pre-pandemic levels of 2019. The bank is witnessing economic activity gaining momentum for large corporates, especially after budget announcements. On the sectoral front, infrastructure, pharma, metals and commodities, cement and materials, food processing and automotives are exhibiting strong growth. The management is also expecting private corporate capex to pick up in the second half of the year.

In the past two years, the bank has faced nearly five outages on its digital and online banking platforms. But it has not impacted its business, yet. Investors and customers are concerned about RBI’s ban on HDFC Bank’s digital initiatives and issuance of credit cards, which might impact market leader’s market share in the near term, and that will be one key factor to watch in the coming quarters.