By Deeksha Janiani

After a forgettable start to the new year, markets are set to swing into action as India’s biggest follow-on offer will hit the floor on January 27. Adani Enterprises, which went public in 1994, seeks to raise Rs 20,000 crore as part of its long-term capital management plan.

Meanwhile, Hindenburg Research, a US-based investment research firm has come out with a detailed report alleging “brazen” stock manipulation and accounting fraud by the Adani Group. In response, the conglomerate said that the report “was timed with malicious intent” to discredit the company ahead of its FPO. But Adani has yet to respond to the details of the allegations, and share prices of group companies like Adani Transmission, Adani Total Gas and Adani Ports fell by over 5% after the report’s release.

Adani Enterprises (AEL) is the flagship company and the incubator of new businesses for the Adani group. The company derives its revenues mainly from trading imported coal in India. It is also working on a green hydrogen ecosystem, data centres, development of airports and roads, digital platforms, defence and industrial manufacturing.

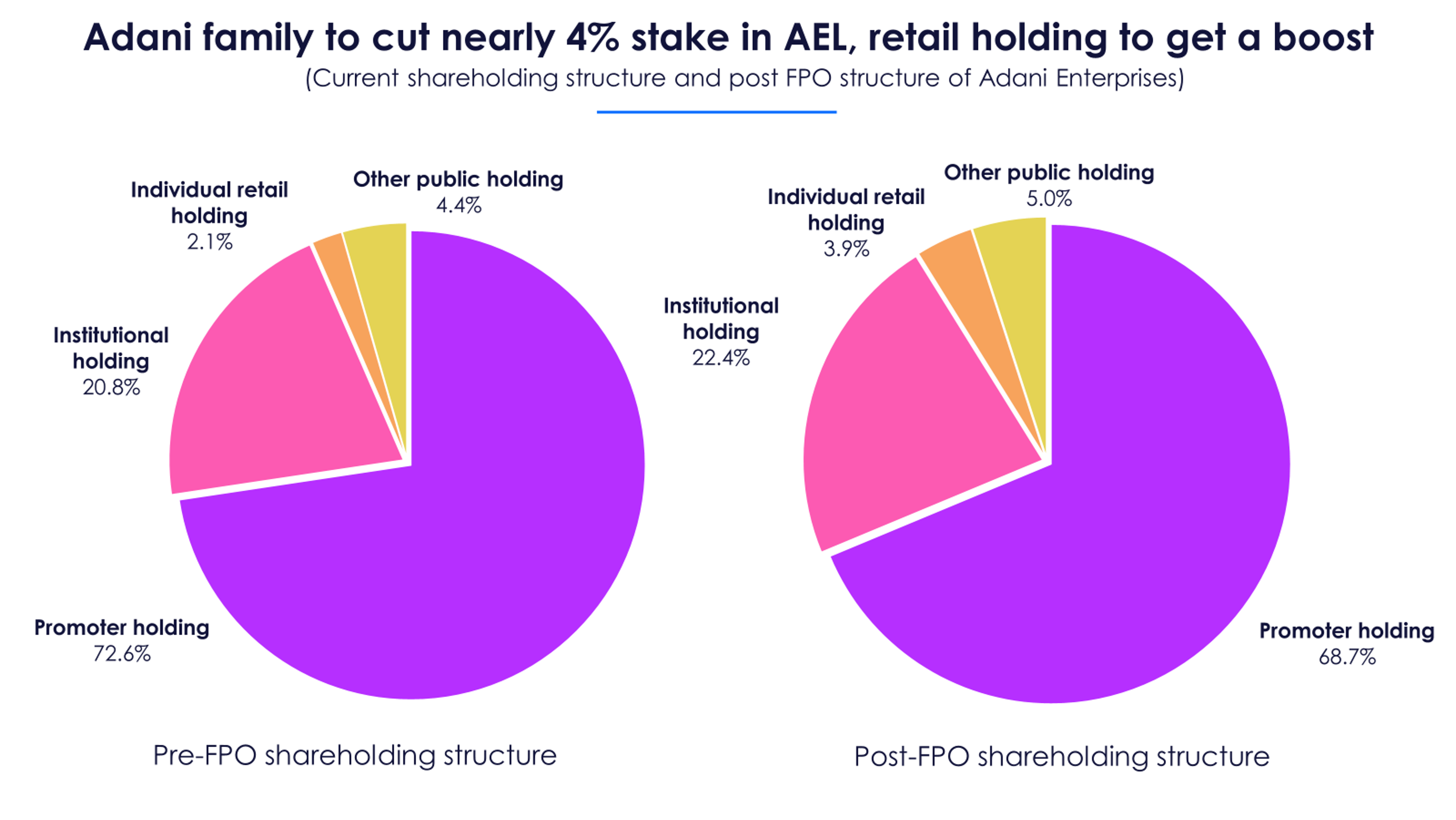

FPO is a bid to enhance the pool of retail shareholders

Prior to this proposed issue, AEL had raised Rs 7,700 crore from an Abu Dhabi-based investment company in May 2022. Now, it seeks to diversify its shareholder base. “Our intention is to expand our share registry with focus on India's retail investors,” as Gautam Adani, chairperson at Adani group, puts it.

The promoter family will reduce around 3.9% stake in the company post this offer. The free float or the shares available for public trading will rise to around 31%. Notably, the stake of individual retail holders will rise by over 1.8X. This is the section of holders who actively trade in the market, unlike institutional holders who tend to sit tight on their investments.

This is expected to improve the trading volumes and liquidity of the stock and its prices will be less prone to wild movements. This could also correct the sky-high valuations of this Adani stock. Notably, the company is issuing partly paid-up shares which will be converted to the main line only after the remaining payment is completed within 18 months.

Major share of proceeds earmarked for energy and infrastructure projects

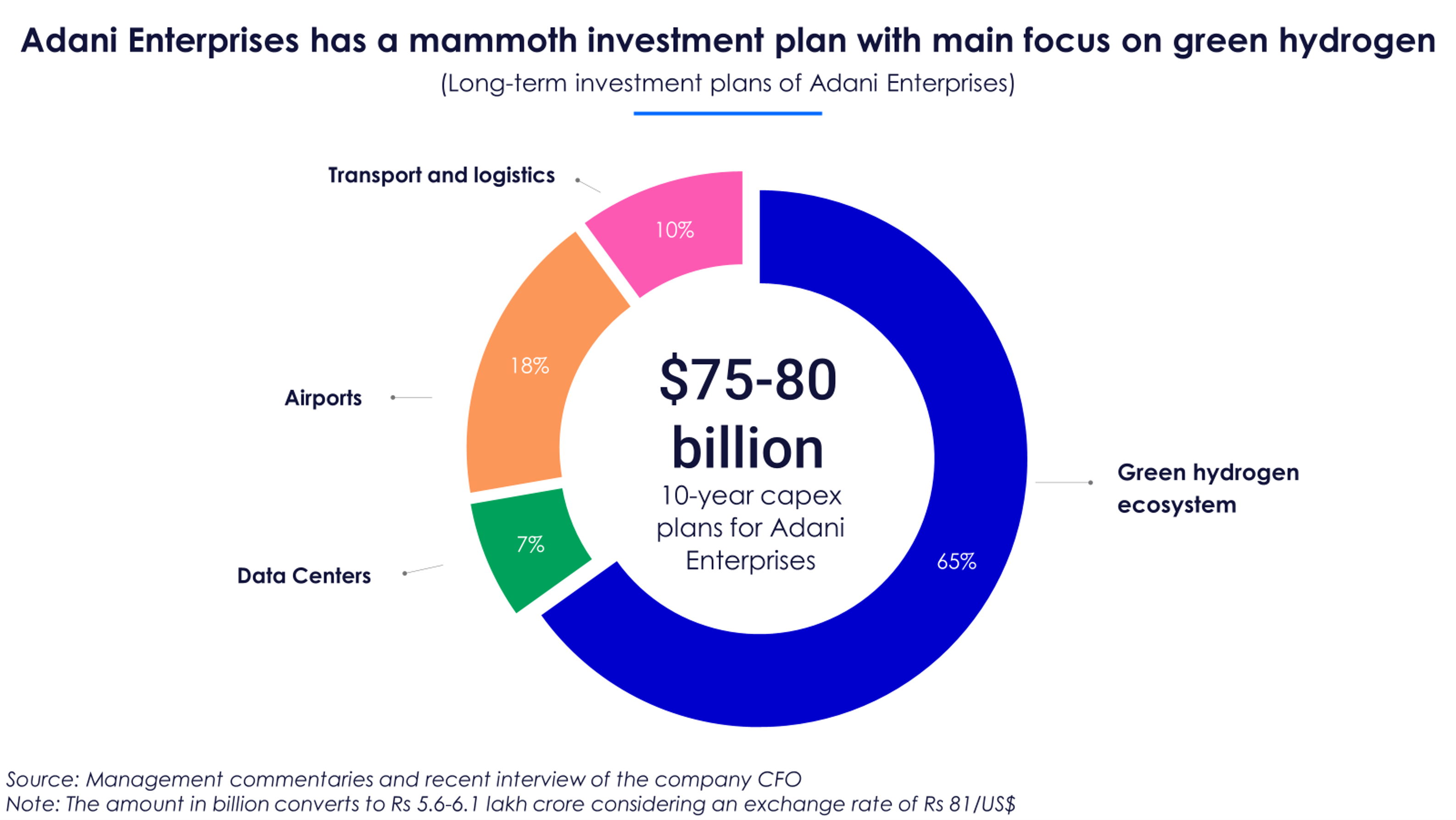

Adani Enterprises intends to utilize over half of the offer proceeds towards its capex projects involving airports, roads and expressways, and the green hydrogen ecosystem. Of the amount set aside for capex, improvement of airports, especially the ones in Ahmedabad and Lucknow, will claim a major chunk.

While this plan is well-intended, the amount earmarked for capital spends looks like a drop in the ocean considering the company’s long-term plans. According to Jugeshinder Singh, Chief Financial Officer at Adani Group, the entire group has a 10-year capex plan of $107 billion, within which AEL has roughly 70-75% share.

A major part of AEL’s investments will go into building the green hydrogen ecosystem. This is a developing technology, which is yet to be proven commercially. Currently, generating hydrogen through renewable energy sources costs twice as much as producing it using natural gas (gray hydrogen). The company will have to build it on a huge scale for it to be viable for the use of heavy industries.

Apart from its capex projects, AEL plans to repay some of its existing debt via the offer proceeds. However, this repayment will reduce the borrowings of the company by only 10%.

On a positive note, the total debt-to-equity metric for AEL will fall below 1X post this FPO.

Adani Enterprises is hard-pressed for free cash with a high debt burden

Adani Enterprises is investing in projects which typically have a long gestation period. Hence, the magnitude of its existing cash flows is important in gauging if it can fund its own growth or if it will continue to require capital infusion.

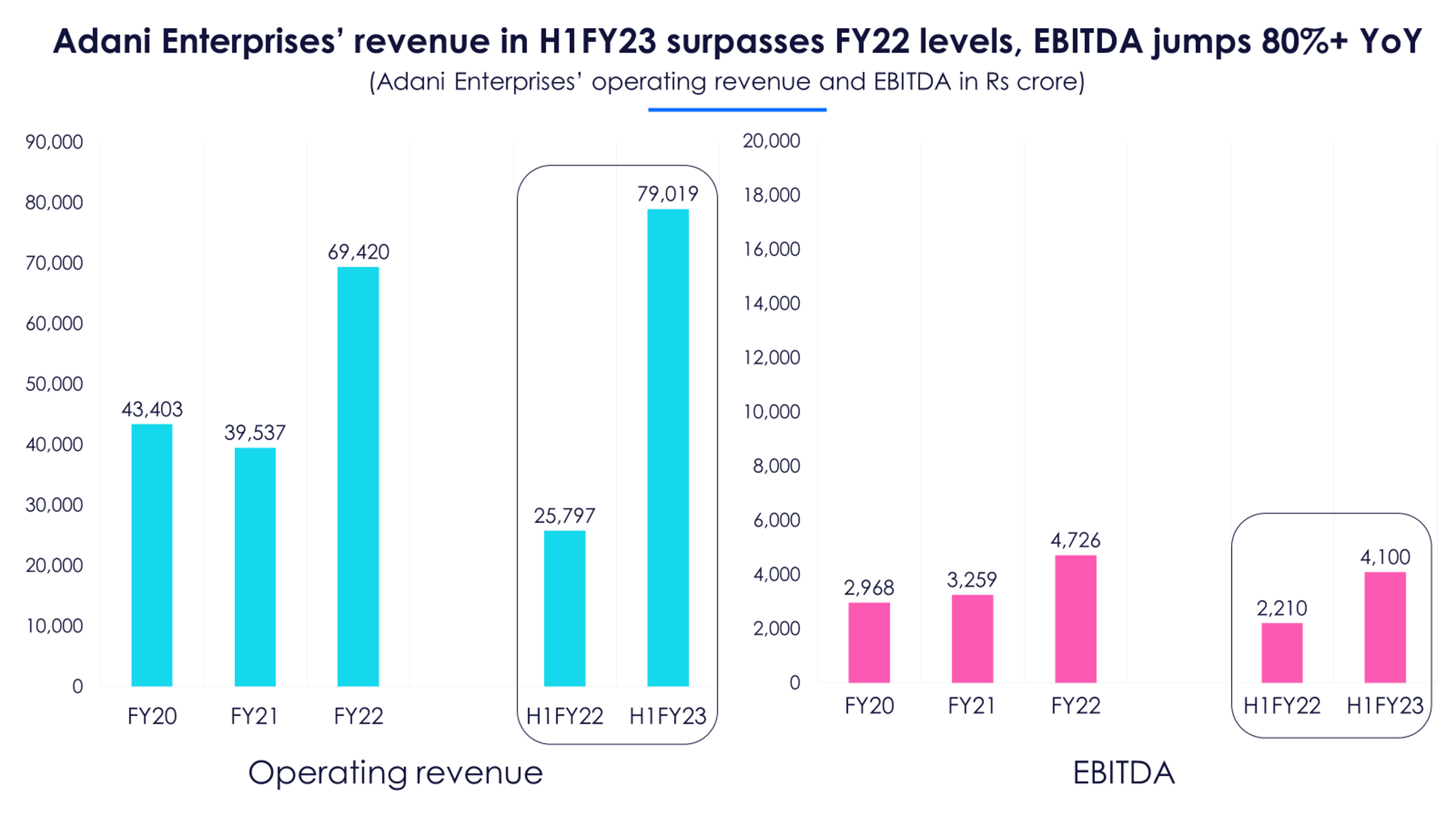

AEL witnessed over 65% fall in its operating cash flows in FY22, owing to an inventory build-up. It also generated negative free cash of over Rs 10,000 crore owing to higher capex. Interestingly, its operating cash improved considerably in H1FY23 due to a jump in operational profits. However, the company was still not able to post positive free cash in this period.

Given AEL’s long-term plans, it should ideally have an annual capex run-rate of Rs 60,000-65,000 crore. This is hard to achieve with its existing cash flows. Hence, it’s possible that AEL may not generate positive free cash for a long time. Its operations won’t make enough cash to pay its financiers or pay dividends to shareholders.

The recent allegations question the accuracy of these accounting numbers itself. The absence of a well-known statutory auditor and the constant attrition among CFOs were some key concerns highlighted in the report.

Rising debt burden is another cause of concern for Adani Enterprises. The company’s net debt to EBITDA ratio rose to alarming levels in FY22, as its borrowings more than doubled. Although it has come down in H1FY23, the metric is still outside the comfort zone. Another red flag is the consistent fall in the interest coverage metric between FY21 and H1FY23.

The management of AEL does not consider its debt level to be a concern despite a declining ability to service it. Its argument is that most of its debt is housed in upcoming businesses, which it plans to demerge anyway.

Adani Enterprises’ fortunes revived in H1FY23

Adani Enterprises’ revenue and EBITDA grew at a CAGR of over 25% between FY20 and FY22. However, its net profits fell by more than 20% in this period. The jump in finance costs and depreciation weighed negatively on the earnings of the company. This is quite natural as the company has continued to expand aggressively with the aid of higher debt.

Interestingly, the company’s operating metrics have improved in H1FY23. Its top line and bottom line in H1FY23 exceeded FY22 levels as well. The flagship division of integrated resource management and the airport segment were the main drivers of this growth.

However, AEL is not able to put its capital to effective use. The company’s return on capital employed has continued to fall and nearly halved to 6.2% between FY20 and H1FY23. This is despite a jump in its operational profits in H1FY23.

At this rate, the company would be better off by putting its capital in a fixed deposit in India. Additionally, it is not able to meet the average cost of capital which was at 11.5% for the infrastructure industry, according to a latest RBSA Advisors’ report. This raises the question if Adani Enterprises is biting off more than it can chew.

A bet on the Indian growth story, but at what cost?

Ahead of the Adani Enterprises’ FPO, Gautam Adani commented on the opportune timing of this issue – “Most of our growth is still ahead of us; our growth plan is aligned with the Indian growth story, with our capabilities and with the needs of India’s retail shareholders.” But the question here is how much are you as an investor shelling out for AEL’s future, not-yet-realized growth.

The offer is priced at a discount of 5-10% for retail shareholders, considering its price bands and the closing price on January 25. However, AEL’s stock will be available at an average PE of over 290X. ‘Pricey’ is an understatement for such a valuation multiple.

Large-cap companies like UPL and Tata Power have high debt levels and posted negative free cash in H1FY23. But, these have a much smaller PE multiple in comparison and generated negative returns in the past year.

Adani Enterprises has an ambitious plan to set up a green hydrogen project of three million metric tonnes, data centres of 1GW and a road portfolio of 12,000 lane km in the next 10 years. It’s indeed dreaming big as it lacks the operational wherewithal to do so.

This FPO might just be the start to a series of equity/debt fundraises that AEL may have to undertake in the future.