By Suhas Reddy

Tata Consultancy Services (TCS) is the first IT company to release its results for Q3FY23, giving investors an early signal into how the rest of the pack may perform in this seasonally weak quarter for IT stocks.

As macroeconomic headwinds still prevail in key markets, Rajesh Gopinathan, CEO of TCS, said in a post earnings press conference that the “overall demand scenario has not changed significantly”. He added, “We’ve gone into December with everybody being cautious. But our view is that this caution has a different colour across markets”.

ICICI Direct anticipates IT companies overall to post moderate sequential revenue growth due to higher furloughs, fewer working days, deferred spending from clients and high inflation. On the other hand, the brokerage expects margin expansion in the range of 10-70 bps QoQ for a majority of companies due to the easing of supply-side pressure, rupee depreciation and lower attrition.

Bellwether TCS kicked off this earnings season with better-than-expected revenue growth, lower attrition and improvement in its EBIT margin. It beat Trendlyne’s Forecaster revenue estimates by 1.5% in Q3FY23.

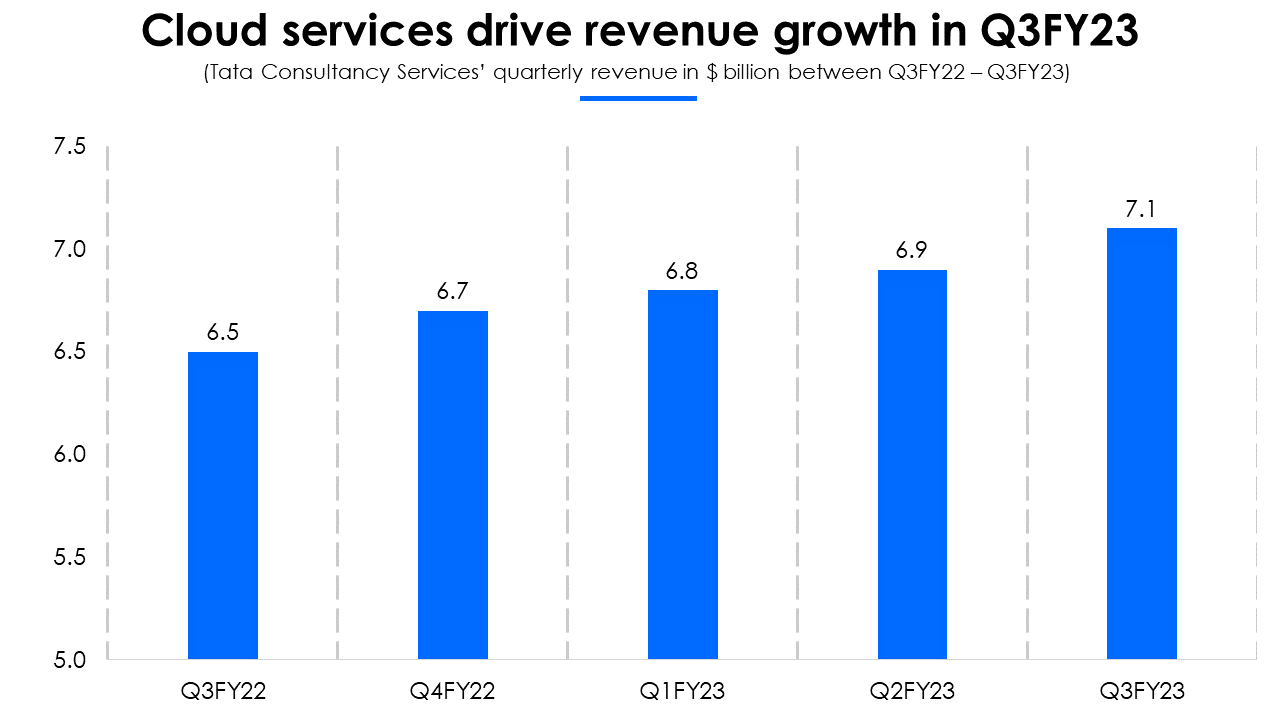

Rajesh Gopinathan attributed the strong revenue growth to “driven by cloud services, market share gains through vendor consolidation, and continued momentum in North America and the UK.”

However, its net profit growth was below expectations, explaining why investors were not enthused by the robust growth in revenue. IT stocks declined on Tuesday, with the Nifty IT falling 0.85%.

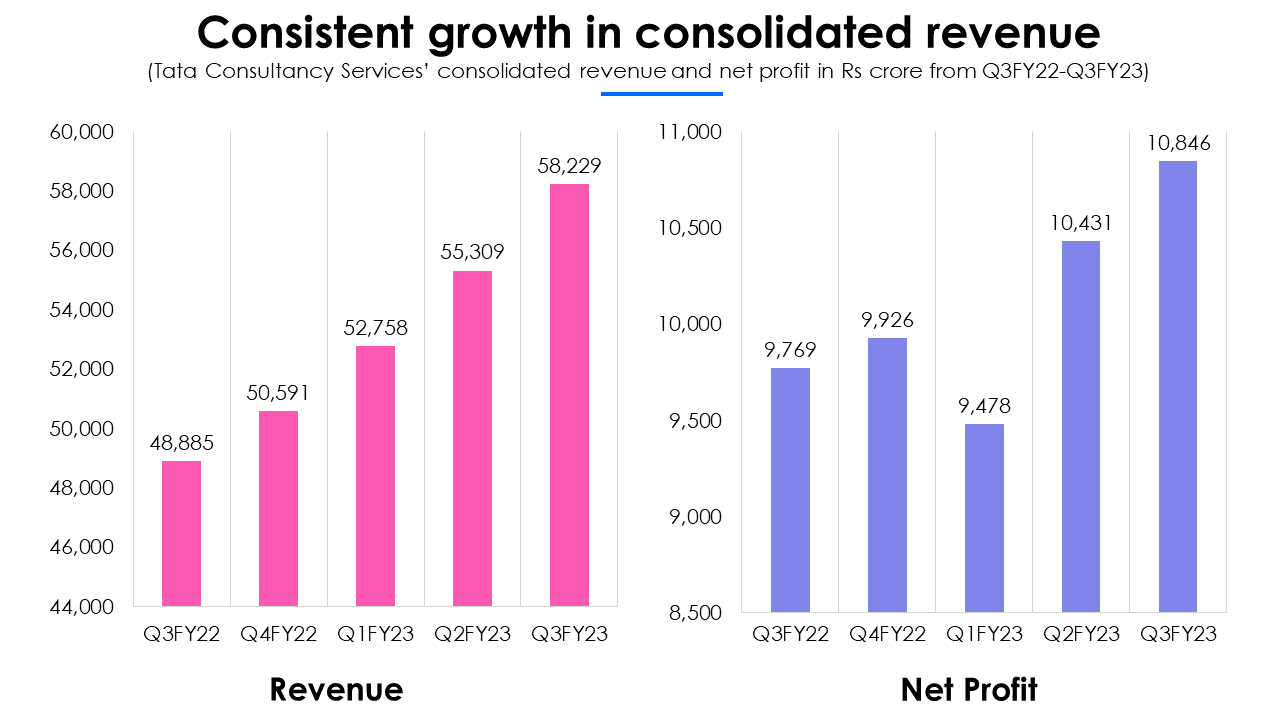

Revenue grows better-than-expected but profit falls short

The IT giant’s revenue grew 5.3% QoQ to Rs 58,229 crore, beating the street’s expectations by a healthy margin in Q3. Its dollar revenues crossed the $7 billion mark, rising by 2.9% QoQ to $7.08 billion. The management attributes the healthy revenue growth to demand for cloud services and market share gains through vendor consolidation.

TCS’ net profit rose for the second consecutive quarter sequentially, rising 4% to Rs 10,846 crore. It missed Trendlyne’s Forecaster profit estimates by 2.1%. This underperformance likely caused TCS shares to close 1% lower at the end of trade on Tuesday.

All the business verticals grew QoQ, with life sciences, manufacturing and retail & consumer business verticals performing well. The company expects the retail vertical to continue its growth momentum in the medium term. However, the management is wary of the manufacturing vertical given the disruptions in global supply chains and energy.

Among key markets, growth was mainly driven by North America and the UK, which together contribute nearly 69% to revenue. While growth in Europe was moderate as clients were more cautious and slowed down decision-making.

Management optimistic about US and UK, cautious on Europe

Going forward, the management is confident about the demand scenario in North America and the UK in the medium term. A short-term slowdown in the US due to inflation is possible, but TCS believes that this is a transient problem and not a structural one. Which makes the firm positive on the US market.

However, the management is cautious about Europe, as the region is grappling with an energy crisis. It believes clarity regarding the business environment will emerge when geopolitical tensions fizzle out in Europe.

As macroeconomic headwinds persist the management believes the overall demand environment has not changed significantly. Therefore, it remains cautious, but the degree of caution varies from market to market. Rajesh Gopinathan added that the three key markets “are moving to three different beats and each of them is indexed to their own specific outlook”.

EBIT margin close to 25%, gains on forex movement

The company’s EBIT margin improved by 50 bps QoQ on account of forex gains, improved utilisation and declining subcontractor costs. The favourable currency movement and operational efficiencies led to a margin improvement of 70 bps and 30 bps, respectively. These were offset by an increase in project-related third-party costs and higher travel expenditures.

The management has an EBIT margin guidance of 25% for Q4FY23, which it aims to achieve through better utilisation, reduction in sub-contractor costs and reduction in attrition. The company also plans to improve pricing to increase margins but acknowledged that given the environment it will prove to be difficult.

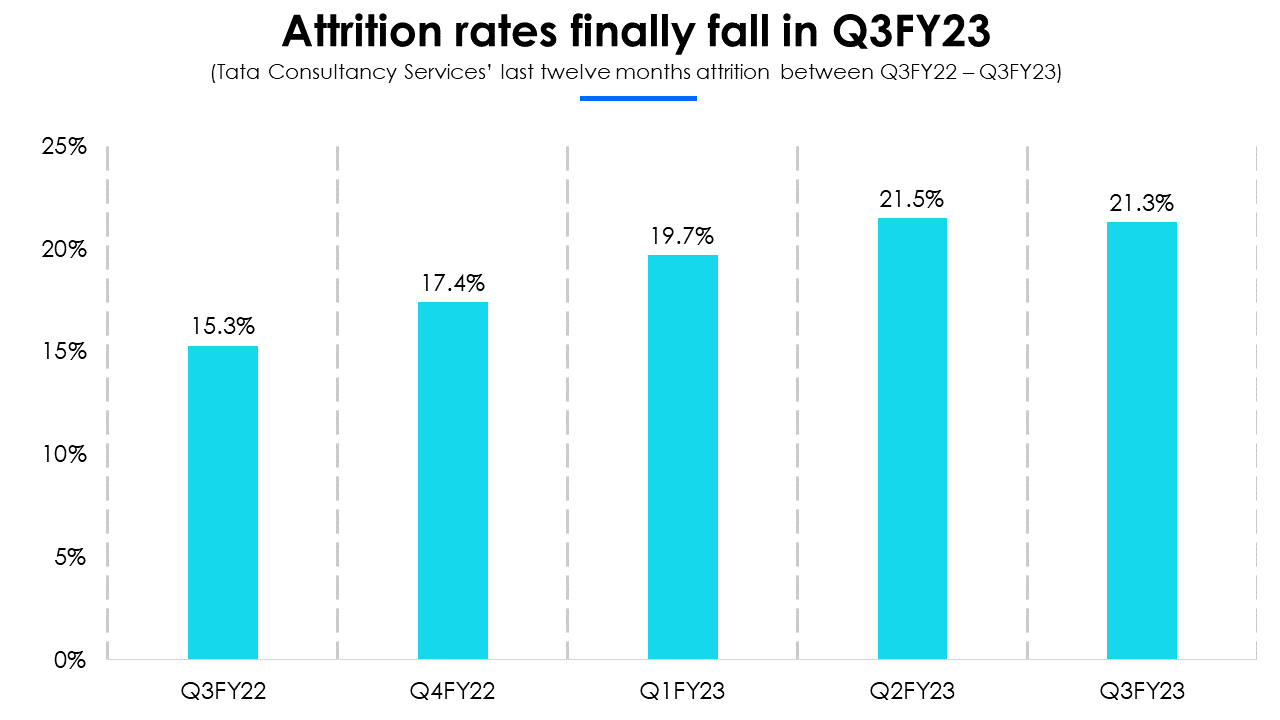

Attrition finally falls after rising for six quarters

With supply-side pressures reducing as the labour market cools off, the company’s attrition has finally declined after rising for six consecutive quarters. Although the decline was marginal, at 20 bps QoQ, it is a positive sign for the company. The other major IT firms like Infosys and Wipro saw their attrition rates decline in Q2FY23.

With the supply of talent improving across the industry, the pressure to poach people has gone down. This is expected to lower the churn further in the coming quarters and push attrition rates down.

Another aspect that partly drove margins up this quarter was the decline in employee costs as a percentage of revenue, which fell 50 bps QoQ to 55.6%. TCS’ employee costs have been declining sequentially since Q1FY23. With worker pay expectations lowering, the wage pressure across the industry is expected to fall.

What came as a surprise was the company reported a net decline in employees sequentially by 2,197. Hiring was also lower, with the company hiring 7,000 freshers in Q3. The management pointed out that the slowdown in hiring is not indicative of a slowdown in demand. It cited better capacity utilisation and improving employee productivity for the fall in employee strength. The net hiring is expected to go back to pre-Covid levels in FY24.

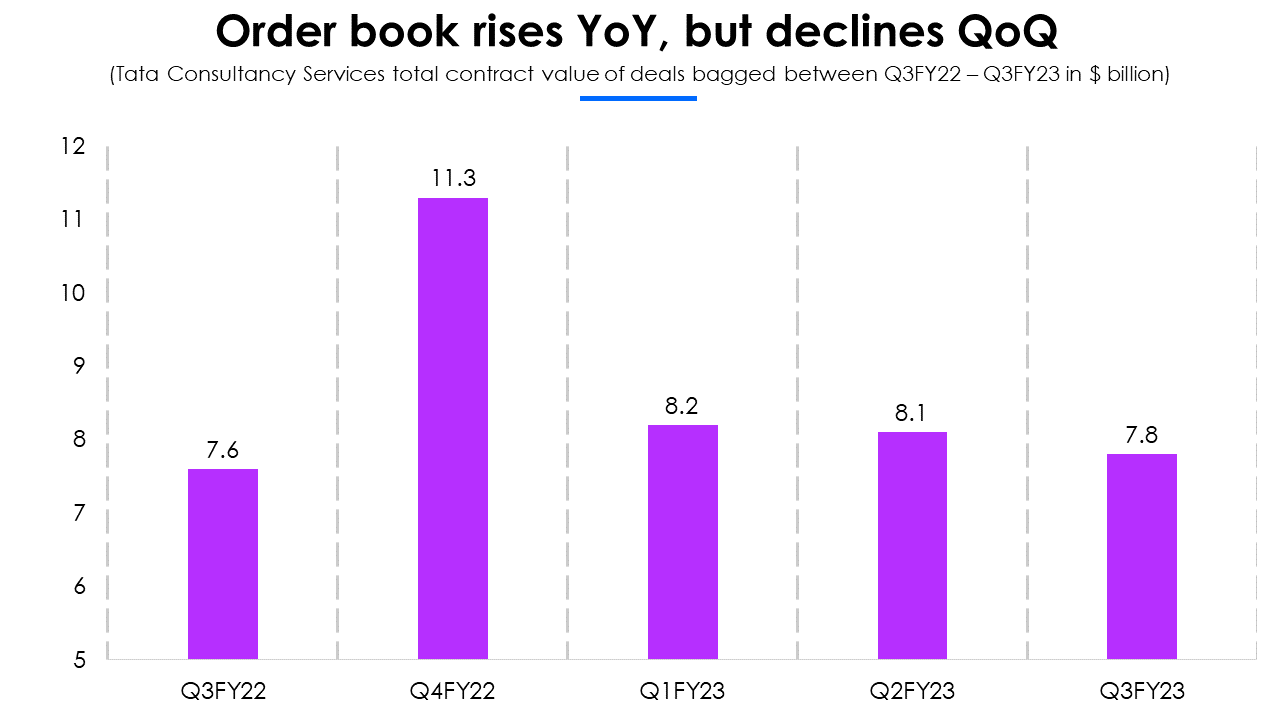

Deal wins remain steady, falls sequentially but rises on a YoY basis

Although TCS’ total contract value (TCV) fell sequentially, it rose on a YoY basis, giving decent revenue visibility for the rest of the year. The TCV for Q3FY23 came in at $7.8 billion, in line with the management’s guidance of $7-9 billion per quarter. The sequential decline in the order book reflects a real slowdown in deal conversions as clients grow cautious.

The company bagged deals worth $2.5 billion in its BFSI vertical and deals worth $1.2 billion in its retail sector. Overall, the deal inflow was healthy across all verticals.

The management expects technology spending on cloud services by its clients across industries to increase in the medium term. Specifically, toward large deals related to cloud transformation. They indicated that spending towards this area will remain stable despite weak macroeconomics, as it is not discretionary in nature.

Demand outlook moderate, margin pressures to ease

The TCS management is fairly optimistic about the company’s performance as it enters the new year. It is upbeat about the demand environment in North America and the UK, which is comfortable for the company, as these two markets make up two-thirds of its revenue.

The North American and the UK markets contribute a significant portion of revenue to many Indian IT companies. This indicates growth in the industry will likely be moderate in FY24.

Given declining attrition rates and improving margins across the board, the worst seems to have passed for the industry. Although, the risk of a slowdown in technology spending still looms given the situation in Europe and inflation in major markets.

This analysis by Trendlyne is meant for investor education - to help understand companies and make informed investment decisions on their own. It should not be considered an investment recommendation.