Flying has become a routine event for millions. Planes are full, airports are busy, and most airlines are finally profitable again after years of recovery. Overall, the global aviation industry looks strong.

But behind these headlines, the industry is seeing some fundamental changes. In many of the largest countries, aviation no longer has a wide field of competitors. Instead, capacity is increasingly concentrated among a handful of large airlines. In some countries, three or four airlines share the skies. In many others, one airline holds a commanding majority share, with another acting as a distant second.

This structure matters because of how it is impacting travellers. People catch a lot of flights, but no one actually likes flying. After the stress of airport security checks, where your favourite shampoo is thrown out if it is in the wrong sized bottle, travellers have to deal with tight legroom, uncomfortable seats, and terrible food.

Where several strong airlines operate, passengers have choice, and at least some options in quality, legroom, and luggage policies. But when one or two airlines control most of the capacity, choices and safety nets disappear, and even a single operational issue can cause turbulence across the entire system, triggering cancellations, delays, and sudden fare spikes for everyday flyers.

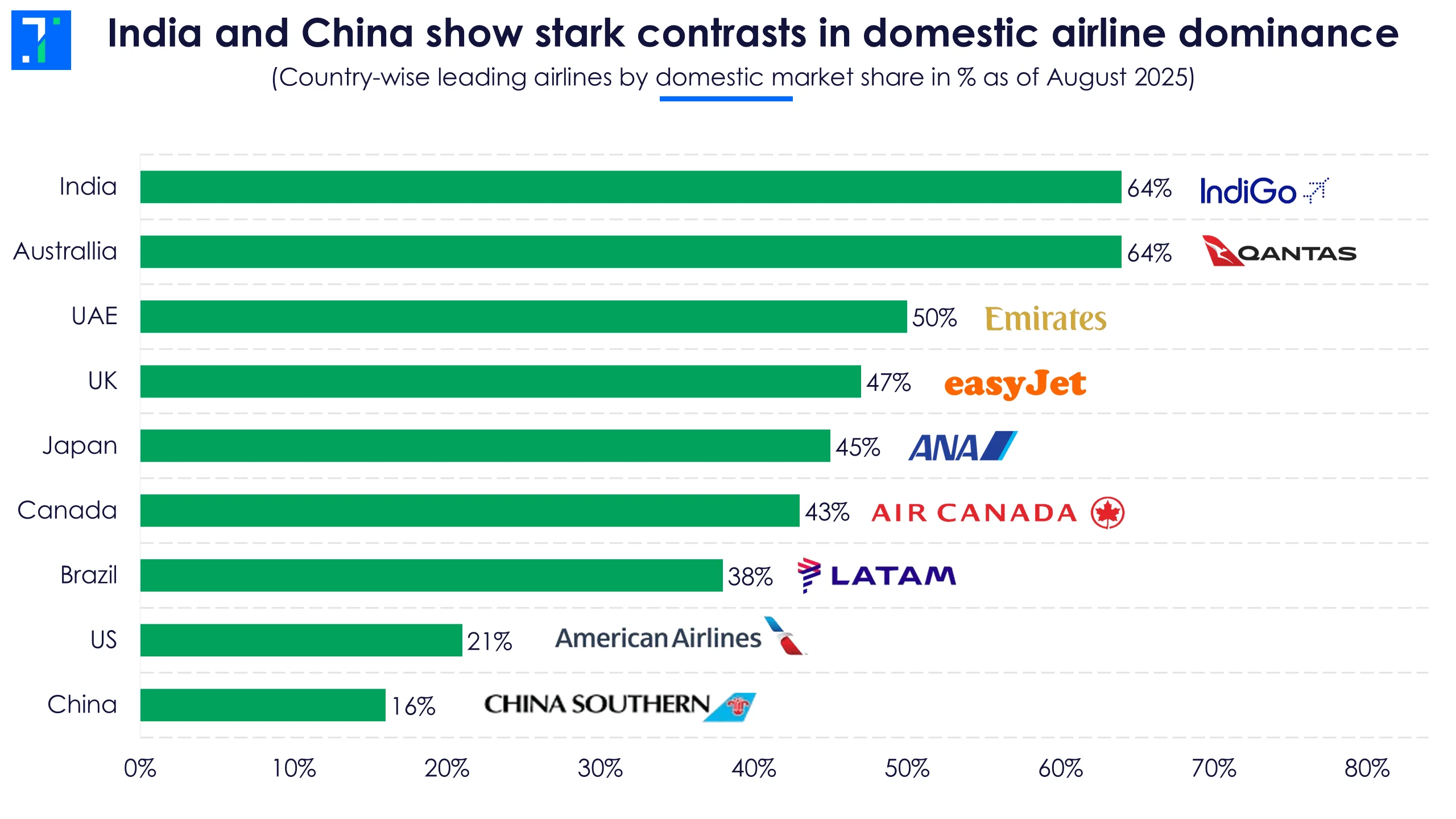

India experienced this first-hand in December 2025. Operational issues at IndiGo, which carries the majority of domestic passengers, caused widespread cancellations. With no large alternative airline to absorb the shock, passengers were stranded, ticket prices on some routes skyrocketed, and the government had to impose fare caps.

“IndiGo’s size has grown to the point where operational setbacks pose systemic risk. If IndiGo or Air India gets into trouble, there will be mayhem in Indian aviation. The government needs to reduce jet fuel taxes and encourage more competition,” said Harsh Vardhan, chairman of Starair Consulting.

Too much flying power, too few players

Some aviation markets today are so dominated by one or two carriers that little room remains for smaller rivals.

India is the clearest example. IndiGo and the Air India Group together control nearly all domestic flights. IndiGo’s growth improved domestic connectivity and helped keep fares competitive, yet this dominance also made the system fragile.

Policymakers in India have acknowledged this challenge. After the IndiGo fiasco, Civil Aviation Minister K Rammohan Naidu remarked, “We need at least five airlines with around 100 aircraft each, so the country is not dependent on one or two carriers. This is essential to avoid monopoly and duopoly.”

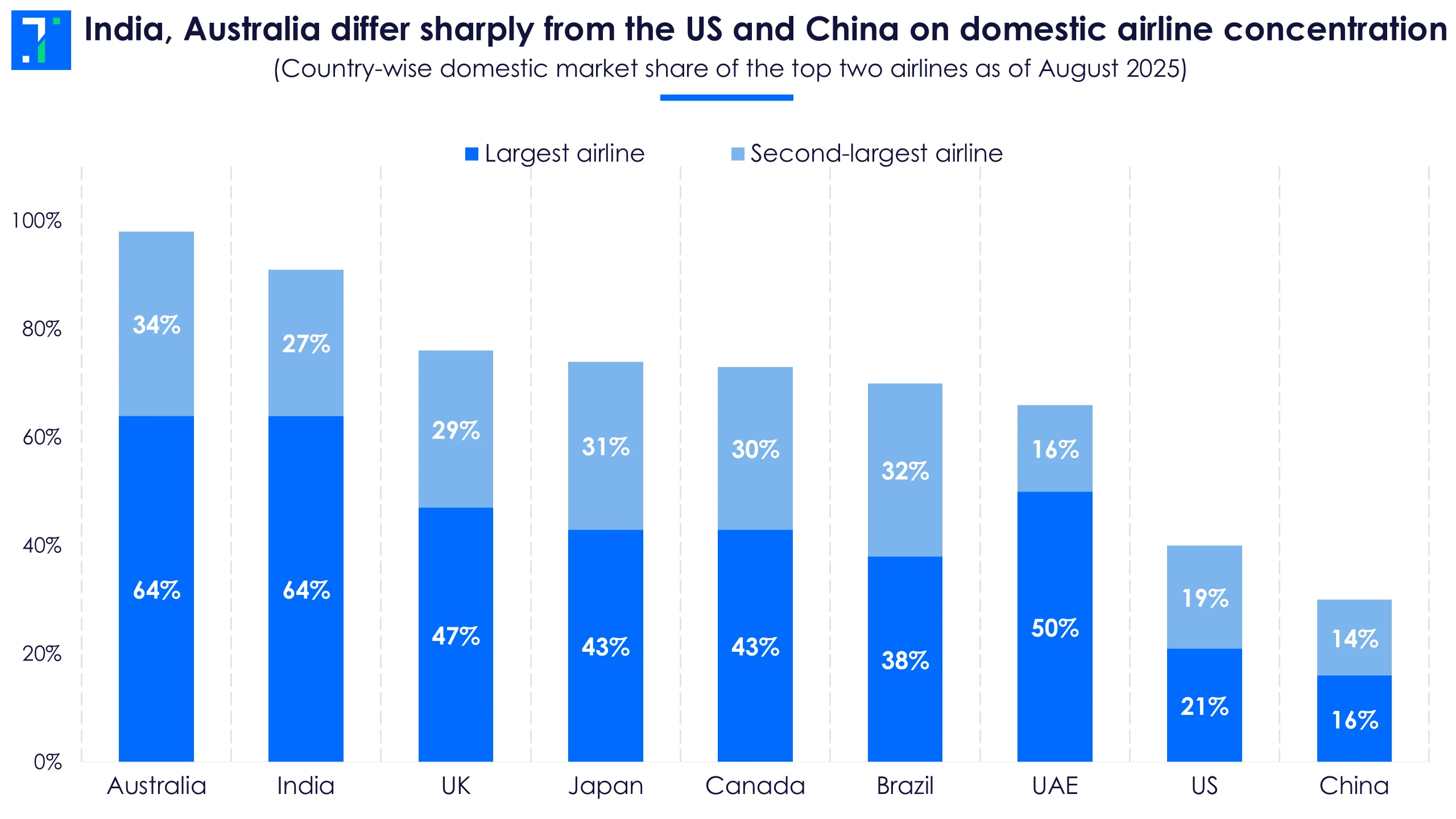

Australia faces a similar problem. The Qantas Group (Qantas Airlines + Jetstar) and Virgin Australia control almost all domestic travel, with smaller carriers barely registering. Recent reports show that these two airlines control over 98% of domestic traffic, leaving passengers with few alternatives and limited bargaining power.

Canada presents another version of the problem. Air Canada and WestJet dominate different regions, and limit direct competition on many routes. A 2025 review pointed to high airport fees and regulatory barriers that protect the existing airlines. This has kept fares elevated and reduced passenger choice.

The UK, while more competitive than these markets, still feels the impact of concentration. EasyJet holds about 47% of total capacity, making it the largest carrier by a wide margin. Rivals like Ryanair and Jet2 provide alternatives, but when major airlines face disruptions, last-minute fares can still rise sharply during peak travel periods.

More airline companies mean fewer system-wide failures

Markets with a few strong competitors—rather than just two—handle crises much better.

The United States is the best example for a non-monopolistic aviation market. Four airlines — American, Delta, United, and Southwest — share most of the market. No single airline dominates completely. This balance prevents system-wide collapse.

North American carriers are competing by boosting premium offerings, with ~90% of widebodies now having premium economy. They are now fighting for customers based on reliability and comfort, not just the cheapest ticket.

Brazil fits here better than it appears at first glance. LATAM Brasil is the largest carrier with roughly 38% market share, but it does not control the market outright. GOL Linhas and Azul together ensure no single airline can dictate pricing unchecked. While competition on major routes is not fierce, the presence of three sizable players provides more stability than a two-airline system.

The UAE represents a different form of oligopoly. Emirates and Etihad dominate the market, but they compete globally rather than just domestically. Emirates is owned by Dubai’s Investment Corporation, alongside flydubai, which serves regional and domestic routes. Etihad is wholly owned by Abu Dhabi’s ADQ sovereign wealth fund.

State backing provides patient capital and strategic staying power, enabling both carriers to compete aggressively with global hubs like Qatar Airways, Lufthansa, and Turkish Airlines. The mix of a few dominant players, strong state support, and layered domestic competition makes the UAE airline market uniquely competitive.

When rails outspeed the skies

Aviation is also more balanced in markets where high-speed rail shares the load.

China’s airline market appears competitive, but high-speed rail has reshaped travel patterns. For journeys under 800 km, trains are faster and easier than flying. On the Beijing–Shanghai corridor, high-speed rail captured about 34% of airline passengers. This forces airlines to focus on longer routes and limits their pricing power on domestic sectors.

Japan looks like a classic two-airline market, which usually means high prices. But Japan is different. The Shinkansen bullet train keeps airlines in check. On routes like Tokyo–Osaka, trains carry over 80% of travellers. Airlines have to offer better service and sharper prices just to stay relevant.

This competition between trains and planes creates a rare result: high reliability and great service without crazy prices. It proves that the best check on an airline monopoly might not be another plane, but a fast train.

What does this mean for travellers?

Rising passenger numbers can hide deeper problems in aviation markets. When most flights are controlled by just a few airlines, even minor disruptions affect the entire system. For travellers, this often means higher fares and minimal options when flights are cancelled or delayed.

Governments are finally taking notice. Fare caps in India and competition reviews in Europe show increasing concern that aviation needs backup options, not just bigger airlines. As travel demand keeps rising, stable air travel will depend on policies that support real competition — through more airlines, easier airport access, and alternatives like high-speed trains.